Neil Garfield writes again on the topic of “servicer advances” today, explaining in a nutshell what they are:

“[Servicer advances] fall into the category of payments made to the creditor-investors, which means that the creditor on the original loan, or its successor is getting paid regardless of whether the borrower has paid or not.”

In short, as Garfield notes, this means that the supposed holder of your note (to the extent that your note was actually and correctly securitized and negotiated, which is unlikely) gets paid on your “obligation” whether you make payments on the note or not.

Here’s how Garfield puts it:

“The Steinberger decision in Arizona and other decisions around the country clearly state that if the creditor has been paid, the amount of the payment must be deducted from the amount allegedly owed by the “borrower” (even if the the borrower doesn’t know the identity of the creditor).

The significance of servicer advances has not escaped Judges and lawyers. If the payment has been made and continues to be made, how can anyone declare a default on the part of the creditor? They can’t. And if the payment has been made, then the notice of default, the end of month statements, the notice of acceleration and the amount demanded in foreclosure are all wrong by definition. The tricky part is that the banks are once again lying to everyone about this.”

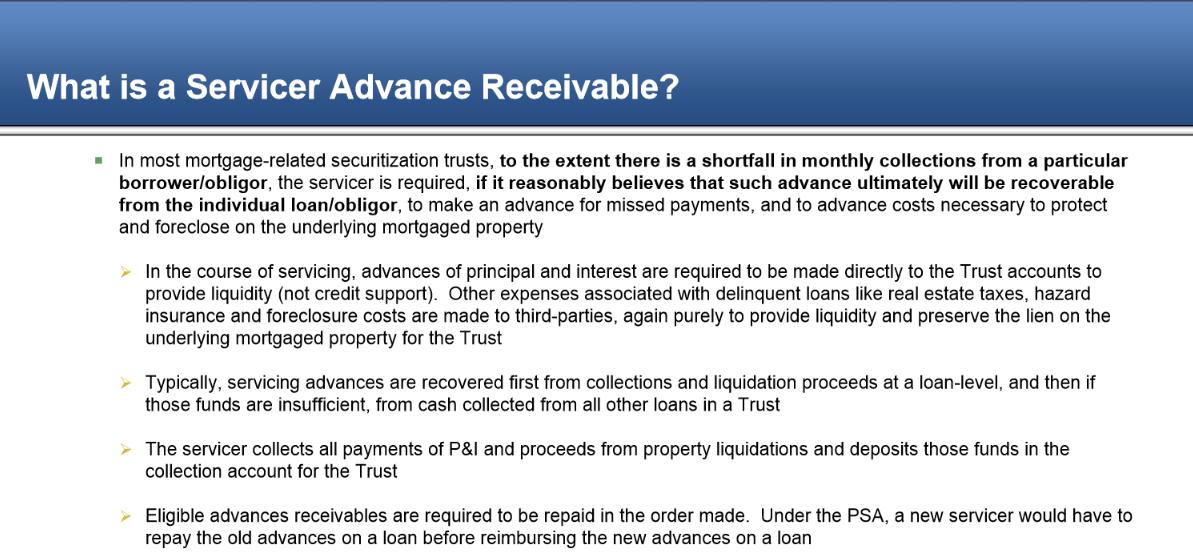

Some commenters on this post take exception to what Garfield is saying here, essentially saying he’s an idiot and doesn’t know what he’s talking about because he mis-characterizes what servicer advances are. Well, if one were to go to Google and simply search “servicer advances” one would be presented with the following as one of the top results, from Ocwen Servicing:

This is from the second page of a 5-page Ocwen document which spends four of those pages discussing servicer advances. And what do those pages say? Pretty much what Garfield argues, though of course not in Garfield’s exact words.

The real question and how mortgage servicers are like the Starbucks drive-thru

So the real question presented by servicer advances is this: if the servicer on my mortgage makes payments to the creditor (again, assuming the un-likelihood securitization and negotiation took place properly or at all) on my behalf but without my knowledge or express consent, why do I owe anybody anything?

The servicer advance agreement is between the supposed creditor and the servicer, not between me and the servicer. I can’t be unjustly enriched by being made party to a scheme–i.e., the servicer making payments even if I don’t–that I don’t even know is happening and that I didn’t directly or indirectly agree to. Where I’m from, if you pay for something for me without my knowledge or agreement, that’s called a gift. That’s called “paying it forward,” like at the Starbucks drive-thru:

“We were impressed when we learned that 450 Starbucks customers in Connecticut paid for the order of the next person in line in a multiple-day chain of generosity. Today, we learned that the chain ultimately continued for a thousand more drive-thru customers, spanning a few days after Christmas.

What kept the chain going was a sort of rolling fund that extra “donations” were added to, and that baristas used when someone rolled up to the window with no one behind them. Presumably, the fund also came into play when someone in line wasn’t interested in playing along.

“It means a lot people are still looking out for other people and being caring and bringing out the holiday spirit,” one customer who joined the chain told NBC Connecticut.”

Now imagine if your Starbucks order had been paid for by someone ahead of you–you didn’t ask them to do it, you didn’t know they were going to do it. Can the person who paid for your order without your knowledge and consent now come back against you and say that you were unjustly enriched because they paid for your order even though you didn’t know they were doing it or agree to them doing it? It’s preposterous. How are servicer advances really any different?

IMPORTANT NOTE/DISCLAIMER: The above article is not legal advice and was not written by an attorney. It is merely a collection of common-sense, rational observations written by a sane, rational layperson with common sense. It is recommended that you consult with an attorney for any and all legal advice and/or action.