Black Knight (formerly LPS, the peddlers of fraudulent mortgage documents) reveals that according to its calculations, mortgage originations are at their lowest level ever. Here’s the Zero Hedge summary of the data:

New mortgage originations fell over 23% month-over-month and a stunning 47% year-to-date according to Black Knight (formerly LPS). As they show in their detailed presentation, with a 65% year-over-year drop, new mortgage originations are at their lowest since their records began and what is perhaps more concerning is prepayment speeds signal further declines are ahead and the ratio of serious deterioration to foreclosure (along with huge numbers of loan mods due to reset) suggest the housing market is anything but recovering fundamentally with the average loan in foreclosure now 2.6 years past due.

People catching on to bank fraud or just broke?

So what accounts for this new low in mortgage origination? Maybe people are finally catching on to the fact that the big banks are essentially criminal enterprises and just don’t want to do business with them. Or maybe people have finally realized, as the Bank of England recently reminded the world, that mortgages are fake–that is, they aren’t “loans” in any common understanding of the usage of that word because banks do not lend deposits, hard money, coins, bills, notes, or any other pre-existing form of money or currency. They just enter digits into a computer database and call that a “loan” that you must pay back with interest.

In fact, it’s worth revisiting one of the most startling (at least to those who adhere to the conventional “wisdom”) quotes from the BoE’s recent press release (which applies to banks all around the world, including the United States) which explain and confirm that banks do not lend deposits or pre-existing money:

“When a bank makes a loan, for example to someone taking out a mortgage to buy a house, it does not typically do so by giving them thousands of pounds worth of banknotes. Instead, it credits their bank account with a bank deposit of the size of the mortgage. At that moment, new money is created.”

No, actually at that moment, you’ve been bamboozled. Hoodwinked. As David Graeber pointed out, this admission–which has never been hidden or secret, it’s just not widely known to the public (because of disinformation, of course)–certainly destroys any rationale for the austerity programs that the banks are trying to enforce. But it also destroys any rationale for not having a complete debt jubilee all across the world and completely restarting with a new system. More on this in a future post.

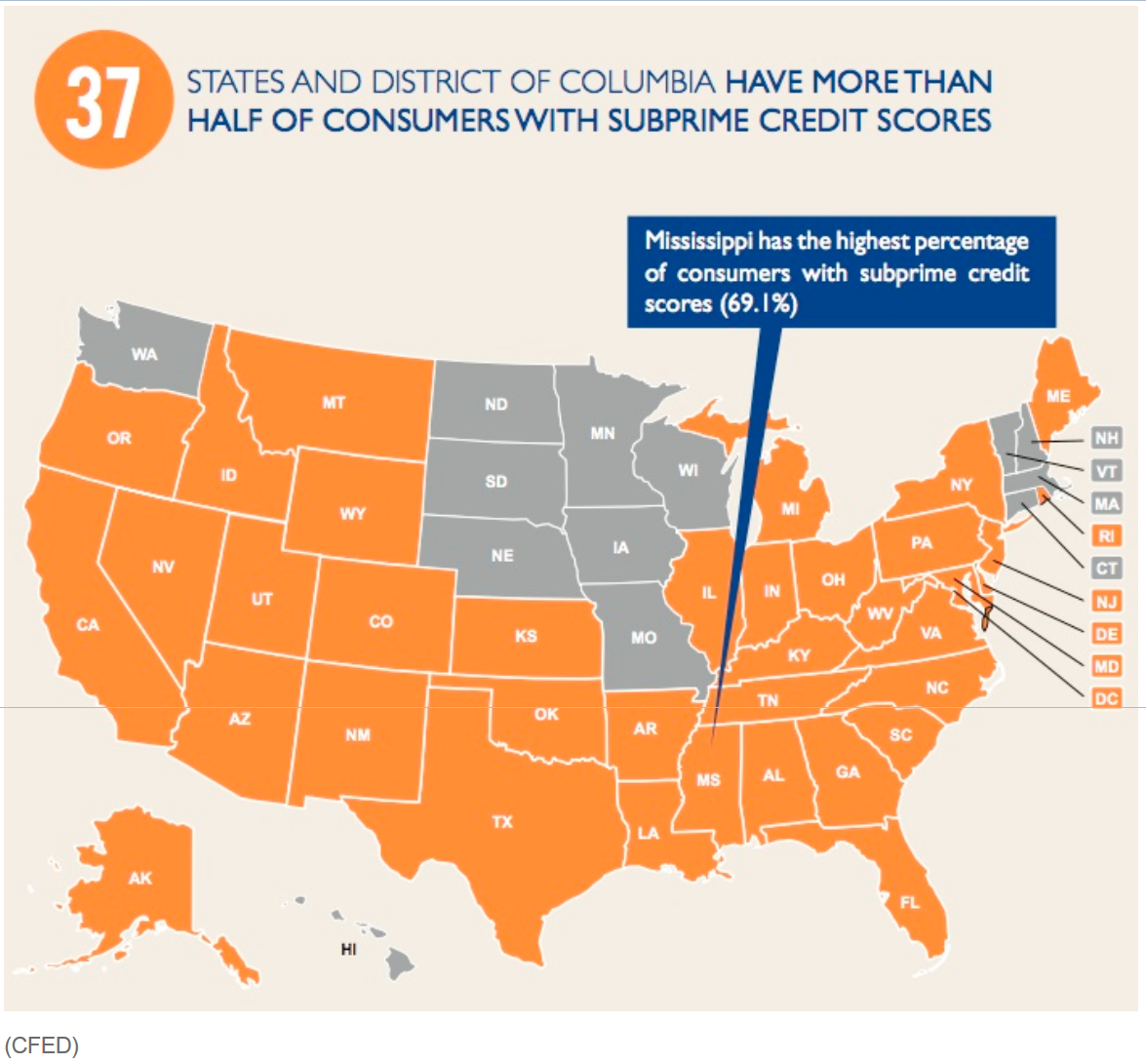

But the more likely answer to the record-low mortgage originations is that people are just broke, unemployed or underemployed, and/or have horrible “credit scores.”

And a credit score by the way, in light of the above info about how money is actually created, is not really a measure of the risk a bank will take in “lending” a person money. That’s because there is no risk for a bank when it “lends” a person money because the banks, as explained above, do not lend money–they enter numbers into a computer and call it a “loan”. But again, that’s a topic for another day. So, I’m going with “bad credit”/broke/un-or-under-employed as the reason for the lack of mortgage originations:

The crooks have possibly gone to far. =) http://4closurefraud.org/2014/04/08/foreclosure-starts-up-mortgage-originations-plunge-to-lowest-on-record/