Apparently Kenneth Rogoff doesn’t think the banks and their kept governments have enough ways to screw us all over, so he is proposing a ban on cash:

“Has the time come to consider phasing out anonymous paper currency, starting with large-denomination notes? Getting rid of physical currency and replacing it with electronic money would kill two birds with one stone.”

I originally wanted to include more of Rogoff’s actual text, but The Financial Times apparently has a hair up its ass about people cutting and pasting, so I’ll play along and just explain the rest in my own words. The two birds that Rogoff thinks should be killed? “Zero bound” interest rates and crime.

That is, he thinks you should have to pay the bank to hold your money, i.e., negative interest. And he thinks you shouldn’t have access to cash because you might buy drugs with it or evade taxes with it.

Rogoff’s replacement for cash? Government-issued electronic currency. But that’s pretty much what we already have, given that the “binary money” (i.e., money that is not cash and essentially only exists in computer databases, i.e., your “checking account”) in existence already is extremely disproportionate to the amount of physical cash:

“Purchases can be made through a Web site, with the funds drawn out of an Internet bank account, where the money was originally deposited electronically. People are earning and spending money without ever touching it. In fact, economists estimate that only 8 percent of the world’s currency exists as physical cash. The rest exists only on a computer hard drive, in electronic bank accounts around the world.“

(Note: According to the Bank of England, it’s actually more like only 3% (p. 2 under “Money Creation In Reality))

So banning cash would only make us more beholden to our banking masters and their kept governments. Which of course is the entire point. Rogoff is pretty clear about this in his article, actually, explaining how his ideas will be of great benefit to central banks and governments without even once wondering about how they might affect the average person.

The real solution

But if, like me, you care about what happens to the average person more than you care about what happens to a central bank and the government it controls, then perhaps you find Rogoff’s ideas as distasteful as I do. But not because I love cash and despise electronic currency.

No, I think what needs to happen is that government/central bank-issued money–whether physical cash or electronic/binary–needs to be eliminated. And at least an Ivy League academic like Rogoff talking about extreme changes to our rapacious financial system makes it seem less weird when I do it…right?

Self-issued currency

I propose that government/central bank-issued money be replaced with self-issued currency. That is, each individual person can issue as much currency as he or she needs to buy whatever he or she wants. And he or she would also have to accept the self-issued currency of others. Sounds crazy, I know, but it’s not. At all. I’ll give you a couple reasons it’s not:

1) Money is already self-issued.

That is, any time you sign a promissory note, you are self-issuing money. That includes loans for real estate, cars, student loans, credit cards, starting a business, getting health care, etc. Indeed, we are taught from birth that if we don’t have enough money for something we need, we have to go to the bank and borrow some. But the bank doesn’t have the money you need either–banks DO NOT “lend” deposits. The bank takes your promissory note and “lends” you “money” for the face value of the note–which most people still somehow vaguely think that means that the bank reaches into its vault and digs out an amount of cash equal to the face value of your note, and puts that “in your account.”

That is not at all what happens. The promissory note you sign over to the bank IS the funding check the bank issues. The note and funding check cancel each other out on the bank’s books. In other words, YOU are creating your own money but being made to treat it as though the bank actually did reach into a vault and dig out the requisite amount of cash which the bank will then have to do without until you pay the “loan” back.

This is all explained very clearly and in no uncertain terms here: “Bank Says: If You Think Banks Lend Deposits, You Are Wrong.”

And a recent press release from the Bank of England described the above this way:

“Commercial banks create money, in the form of bank deposits, by making new loans. When a bank makes a loan, for example to someone taking out a mortgage to buy a house, it does not typically do so by giving them thousands of pounds worth of banknotes. Instead, it credits their bank account with a bank deposit of the size of the mortgage. At that moment, new money is created. For this reason, some economists have referred to bank deposits as ‘fountain pen money’, created at the stroke of bankers’ pens when they approve loans.

This description of money creation contrasts with the notion that banks can only lend out pre-existing money, outlined in the previous section. Bank deposits are simply a record of how much the bank itself owes its customers. So they are a liability of the bank, not an asset that could be lent out. A related misconception is that banks can lend out their reserves. Reserves can only be lent between banks , since consumers do not have access to reserves accounts at the Bank of England.”

2) Money is already worthless.

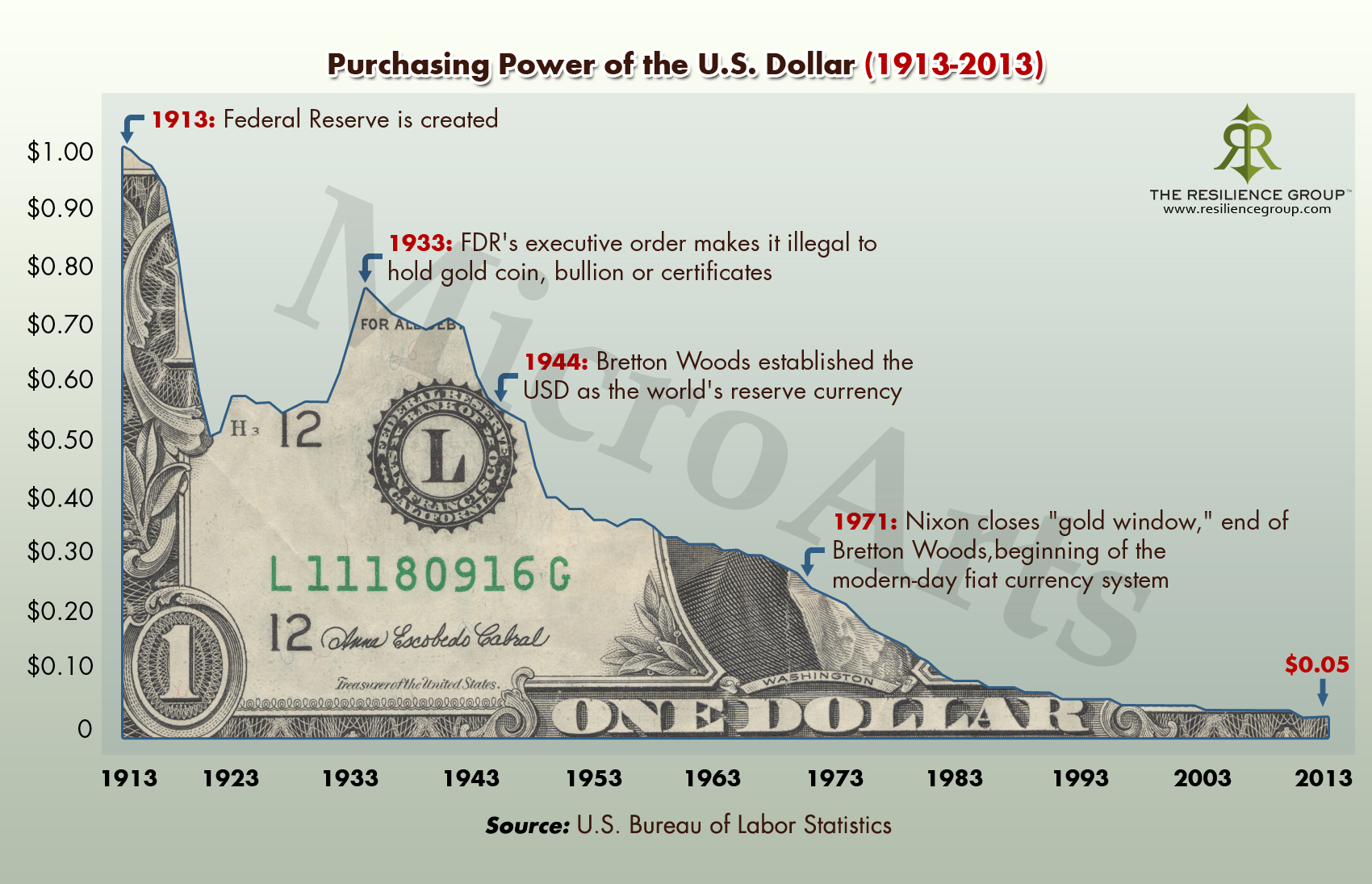

The U.S. dollar has lost, by most estimates, 95-98% of its 1913 value (that date being significant because that’s when the Federal Reserve was born and was the last year the U.S. monetary system was not polluted by central bank chicanery). That 2-5% of value left in the dollar exists only because we average people keep using it because we don’t really have much other choice at the moment.

Some might say, “Well, prices have gone up, so of course the dollar has lost some purchasing power since 1913–that’s over 100 years ago.” True, but prices have gone up as result of inflation, not because things are worth more now than they were then. For example, a steak dinner in 2014 costs way more than it did in 1913–but it’s still just cow meat and potatoes. Why do cow meat and potatoes cost so much more in 2014 than they did in 1913? Because the dollar is now worthless or near-worthless.

Because even though you can still buy things with dollars, you can’t buy nearly as much as you could in the past with the same amount of dollars.

This wouldn’t be a problem with self-issued currency, because although self-issued currency would be worthless just like our currency is now, inflation would not be an issue.

More on all this later, including the fact that I should have mentioned above in point #2 that money is only given value by our belief that it has value. And I wanted to comment on the “dilemma of something for nothing,” but I have run out of time…

The banks create an image in your mind, the banks control you, if you believe the King has invisible clothes. I am sure the banks would frown on bartering and trading like the old days. Bipassing the need for the banks at all. Tear up your credit cards if you have not already. Purchase only what you can afford out of pocket or barter or trade. Cut the banks out if at all possible in all ways you can. The banks are securitizing your credit cards. Basically in my opinion securitizing means using the credit cards for criminal intent. Selling the money out of thin air to investors, stealing and pilfering from pension funds etc. The banks have found a way to continually steal the wealth. Electronic anything, mortgages, currency, you name it, is organized robbery. In my unprofessional opinion.

Right on. Exactly. You mentioned this: ” Selling the money out of thin air.” To me, this is the crux of the whole thing and it’s why I suggest the self-issued currency. Since at least 1971 (Nixon Shock) we have been living with money that is completely fake and as you say, sold to us out of thin air. We’ve been sold nothingness. It is literally the emperor’s new clothes–just as he had no clothes, there is no money. It’s completely made up. And I don’t mean figuratively–it’s literally an illusion, but we are all slaving away for it and people are killing themselves over it. This madness HAS GOT TO STOP. And the simplest way, it seems to me, is to take the power of “money-creation” away from the banks and give it to the people, who are the ones who actually do create the money and give it value.