But don’t take my word for it that everything is a hoax, an illusion. Read this litany from Paul Craig Roberts, former Assistant Treasury Secretary under Reagan, former Wall Street Journal editor, etc.:

“As I write I cannot think of one thing in the entire areas of foreign and domestic policy that the US government has told the truth about in the 21st century. Just as Saddam Hussein had no weapons of mass destruction, Iran has no nukes, Assad did not use chemical weapons, and Putin did not invade and annex Crimea, the jobs numbers are fraudulent, the unemployment rate is deceptive, the inflation measures are understated, and the GDP growth rate is overstated. Americans live in a matrix of total lies.”

Read that last part again: “Americans live in a matrix of total lies.” No, it’s not just you. Yes, things are as bad as they seem. Don’t be ashamed to let on the way you feel. If you cop to it, that encourages others to do the same. Soon, we’re all talking about the problem, and that’s the first step to actually fixing it.

Roberts continues:

“What can Americans do? Elections are pointless. Presidents, Senators, and US Representatives represent the interest groups that provide their campaign funds, not the voters. In two decisions, the Republican Supreme Court has made it legal for corporations to purchase the government. Those who own the government will decide what it does, not those who vote.

All Americans can do is to accept the serfdom imposed on them or take to the streets and stay in the streets despite being clubbed, tasered, arrested, and shot by the police, who protect the power structure, not the public.

In America, nothing is done for the public. But everything is done to the public.“

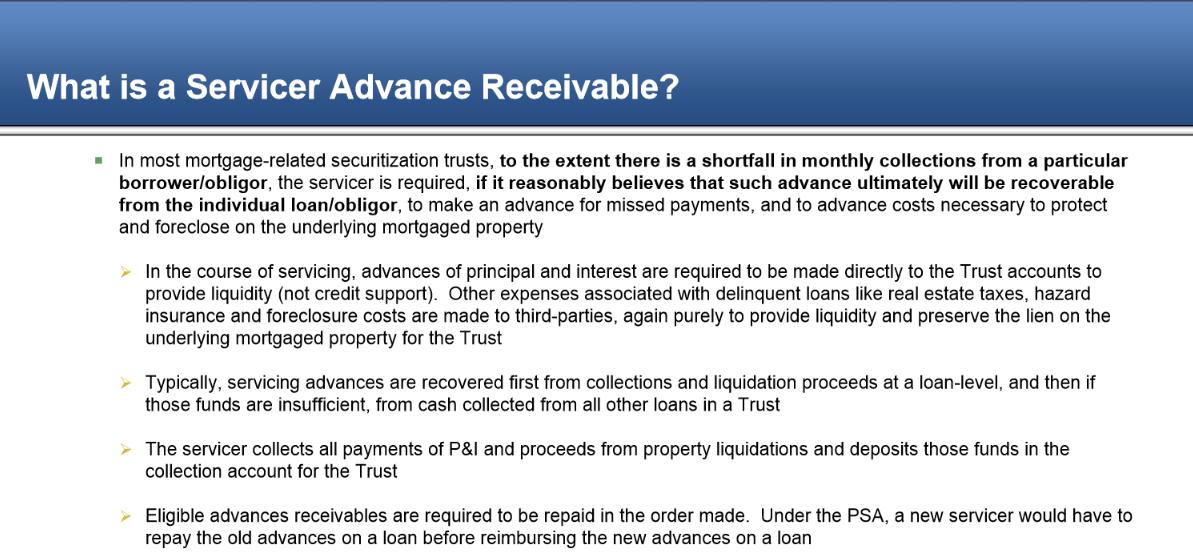

Neil Garfield writes again on the topic of “servicer advances” today, explaining in a nutshell what they are:

“[Servicer advances] fall into the category of payments made to the creditor-investors, which means that the creditor on the original loan, or its successor is getting paid regardless of whether the borrower has paid or not.”

In short, as Garfield notes, this means that the supposed holder of your note (to the extent that your note was actually and correctly securitized and negotiated, which is unlikely) gets paid on your “obligation” whether you make payments on the note or not.

Here’s how Garfield puts it:

“The Steinberger decision in Arizona and other decisions around the country clearly state that if the creditor has been paid, the amount of the payment must be deducted from the amount allegedly owed by the “borrower” (even if the the borrower doesn’t know the identity of the creditor).

The significance of servicer advances has not escaped Judges and lawyers. If the payment has been made and continues to be made, how can anyone declare a default on the part of the creditor? They can’t. And if the payment has been made, then the notice of default, the end of month statements, the notice of acceleration and the amount demanded in foreclosure are all wrong by definition. The tricky part is that the banks are once again lying to everyone about this.”

Some commenters on this post take exception to what Garfield is saying here, essentially saying he’s an idiot and doesn’t know what he’s talking about because he mis-characterizes what servicer advances are. Well, if one were to go to Google and simply search “servicer advances” one would be presented with the following as one of the top results, from Ocwen Servicing:

This is from the second page of a 5-page Ocwen document which spends four of those pages discussing servicer advances. And what do those pages say? Pretty much what Garfield argues, though of course not in Garfield’s exact words.

The real question and how mortgage servicers are like the Starbucks drive-thru

So the real question presented by servicer advances is this: if the servicer on my mortgage makes payments to the creditor (again, assuming the un-likelihood securitization and negotiation took place properly or at all) on my behalf but without my knowledge or express consent, why do I owe anybody anything?

The servicer advance agreement is between the supposed creditor and the servicer, not between me and the servicer. I can’t be unjustly enriched by being made party to a scheme–i.e., the servicer making payments even if I don’t–that I don’t even know is happening and that I didn’t directly or indirectly agree to. Where I’m from, if you pay for something for me without my knowledge or agreement, that’s called a gift. That’s called “paying it forward,” like at the Starbucks drive-thru:

“We were impressed when we learned that 450 Starbucks customers in Connecticut paid for the order of the next person in line in a multiple-day chain of generosity. Today, we learned that the chain ultimately continued for a thousand more drive-thru customers, spanning a few days after Christmas.

What kept the chain going was a sort of rolling fund that extra “donations” were added to, and that baristas used when someone rolled up to the window with no one behind them. Presumably, the fund also came into play when someone in line wasn’t interested in playing along.

“It means a lot people are still looking out for other people and being caring and bringing out the holiday spirit,” one customer who joined the chain told NBC Connecticut.”

Now imagine if your Starbucks order had been paid for by someone ahead of you–you didn’t ask them to do it, you didn’t know they were going to do it. Can the person who paid for your order without your knowledge and consent now come back against you and say that you were unjustly enriched because they paid for your order even though you didn’t know they were doing it or agree to them doing it? It’s preposterous. How are servicer advances really any different?

IMPORTANT NOTE/DISCLAIMER: The above article is not legal advice and was not written by an attorney. It is merely a collection of common-sense, rational observations written by a sane, rational layperson with common sense. It is recommended that you consult with an attorney for any and all legal advice and/or action.

Charles Hugh Smith gets it exactly right in this excerpt below. The emperor is naked, and you can see it with your own eyes, if only you will open them and wake up! Smith’s commentary:

The stock market is only the tip of the iceberg of what’s being rigged. For a taste of what’s rigged, ask yourself this question: if Mr. Elite Insider perpetrates a scam, and Mr. John Q. Citizen breaks similar laws, is there any difference between the treatment each receives?

Let’s go even deeper and ask: why is looting legal, even though it is obviously crooked? Why is high-frequency trading legal? Why is it legal for the Fed to offer money at 0% to its buddies but not to Mr. John Q. Citizen?

Why is it legal to issue student loans to future debt-serfs that is unlike all other debt in that it cannot be discharged in bankruptcy?

Since the legal looting continues unabated regardless of what party or toady is in office, then what actual difference is there between the Demopublicans and Republicrats?

It’s not just the stock market that’s rigged–the entire Status Quo is rigged. There are two sets of laws and two sets of opportunities: one for those holding the concentrated wealth and power, and the other for the rest of us debt-serfs.

If the system isn’t rigged, then why are insolvent banks and bankers protected from the creative destruction of capitalism that befalls John Q. Citizen when his risky bets go bad? Why do we as a nation keep insisting the Emperor’s new clothes are splendid when he is in fact parading around buck-naked?

The only thing I’d add to Smith’s commentary? Money is fake, fictional, created out of thin air. There is no spoon, my friends! We are indeed living in a fairy tale–the Matrix is not just in a movie…

Stock market: rigged. Money: out of thin air. Wall Street bonuses: more than all federal minimum wage employees combined. The pattern recognition skills of the public have GOT to be kicking in by now, yes?

EVERYTHING. IS. RIGGED.

From Zero Hedge (discussing high-frequency trading with “Flash Boys” author Michael Lewis):

Lewis explains the game, exposes the rigging, and slams the mainstream media’s “defense” of this…

LEWIS: So of course the tourists get fleeced all the time in the poker games, because they don’t know the deck is rigged. The poker players pay the casino a cut of what they make. The casinos, operators, pay the tour group – the tour group company money to bring in the tourists.

So in this case, casino’s the exchange, the poker players are the high-frequency traders, and the tour group operators are the banks and the brokers that handle the stock market orders. And I think the analogy is pretty close. So is that rigged? Is that a rigged game? I think it is a rigged game.

SCHATZKER: Well, it’s rigged only inasmuch as…

LEWIS: Why are you so invested in the idea this is fair? Why are you even arguing about this? It’s so clear.

SCHATZKER: Me?

LEWIS: Yes, you seem to be. I mean, it’s very interesting. But you seem to be – you can see, it’s very clear that people are being front run in the market. There’s plenty of evidence in the book.

SCHATZKER: Their orders are being anticipated…

LEWIS: Anticipated and run in front of, that’s right.

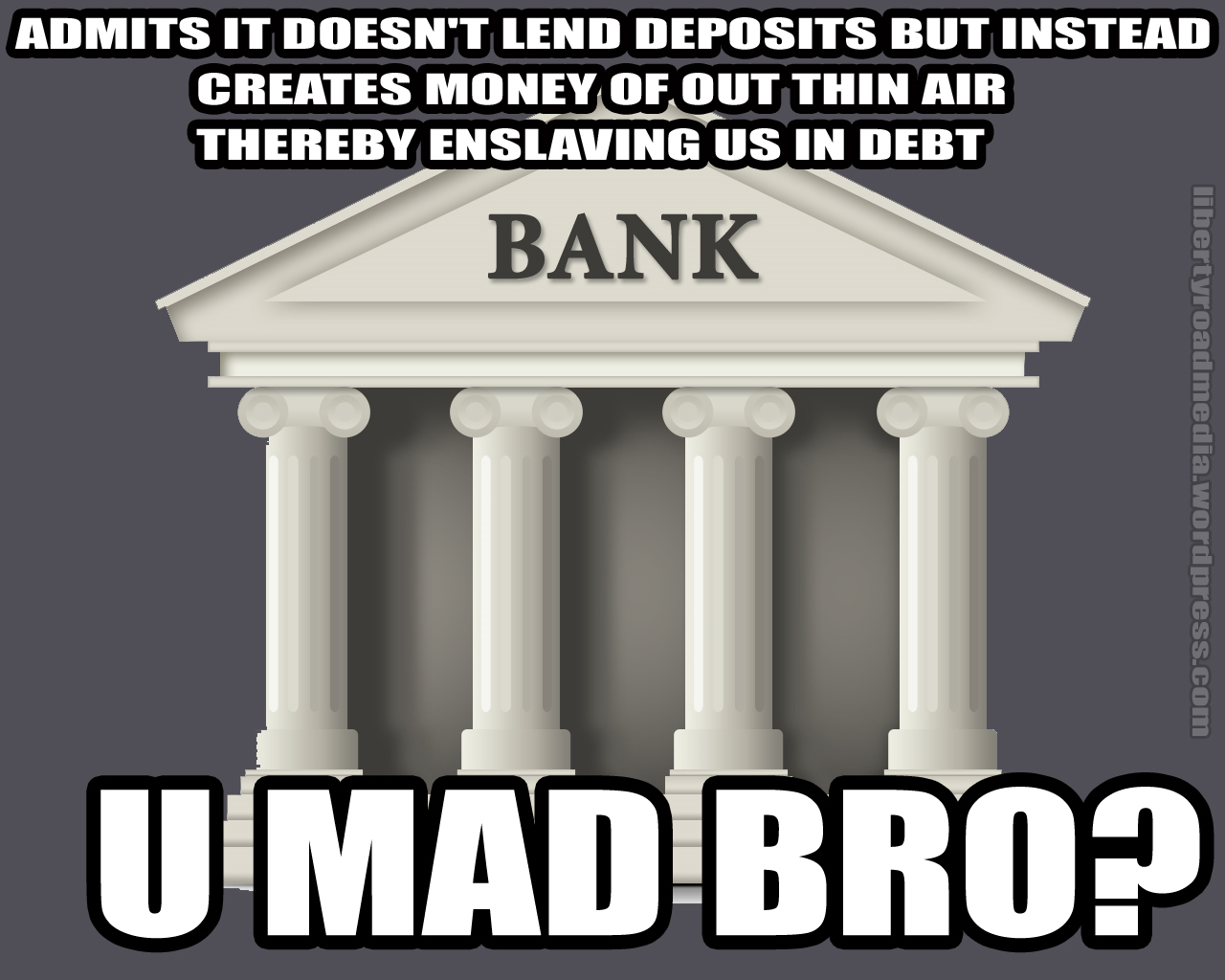

This is NOT an April Fool’s prank. Indeed, the Bank of England wants you to understand that when it comes to money creation, everything you “know” is wrong (cross-posted at The Air Standard)…

In its recent press release, the BoE takes great pains to point out that the way money is really created is: 1) the opposite of what most (almost all) people believe, which is that banks lend deposits or excess reserves or pre-existing money—none of that is true—and 2) contrary to, indeed, the “reverse” of what “some economics textbooks” say.

The BoE wants to be clear about this, then, and get us all on the same page, and that page is that banks make up money out of thin air and “lend” it to you, which is an absurdity and an insult on its face. The BoE wants to be sure you understand that banks are “loaning” you made-up money that they do not have because somehow, you got the damn-fool notion that they loan out deposits instead of funny money. Oh, you probably got that notion from one of those dreadful textbooks in your government school. Pish posh, old chap, that was a bloody lot of nonsense, stories for boys and all. Pip pip cheerio and all that rot.

The info from the BoE applies to all banks, including those in the United States

And we should add here that although this press release comes from the Bank of England, the statements it makes about money creation apply to all commercial banks in modern economies, including the United States. Indeed, the press release references material from former Federal Reserve chair Ben Bernanke, a publication from the Minneapolis Fed, and a 1963 article written by the late James Tobin, a Yale economics professor. Just making that clear for those who might wish to dismiss these mind-boggling statements as being exclusive to the Bank of England.

So here is a choice quote from the press release regarding point 1) above, which is that while most people believe that banks lend out deposits, they are wrong:

“One common misconception is that banks act simply as intermediaries, lending out the deposits that savers place with them. In this view deposits are typically ‘created’ by the saving decisions of households, and banks then ‘lend out’ those existing deposits to borrowers, for example to companies looking to finance investment or individuals wanting to purchase houses.”

So it is both “common” and a “misconception” that banks lend out “the deposits that savers place with them.” I’ll say it again—the central bank itself says that banks do not lend out deposits. That’s not my opinion, it’s not conjecture, it’s not made up. Banks do not lend money that existed prior to your asking to “borrow” it. The press release explains:

“Indeed, viewing banks simply as intermediaries ignores the fact that, in reality in the modern economy, commercial banks are the creators of deposit money.”

Economics textbooks as mind control devices

But why does the idea that banks lend out deposits exist since that’s not actually what happens at all? Could it be because of those inaccurate textbooks floating around out there? That brings us to point 2) above, regarding what the textbooks got wrong (oopsie!). From the press release:

“This article explains how, rather than banks lending out deposits that are placed with them, the act of lending creates deposits — the reverse of the sequence typically described in textbooks.(3)”

So the BoE would have us believe that the textbooks somehow, inexplicably got it wrong regarding money creation. Yet those textbooks were used to teach people that banks lend deposits, which of course explains how people came to have the “misconception” (the bank’s words, not mine) that banks lend out deposits. However, the fact that banks do not lend out deposits has never been hidden, exactly. It just hasn’t been taught to you. Or me. It wasn’t hidden because footnote (3) in the above quote notes that:

“There is a long literature that does recognise the ‘endogenous’ nature of money creation in practice. See, for example, Moore (1988), Howells (1995) and Palley (1996).”

So in their academic tomes that generally only they read—the insiders, the ones really in the know—they’re quite honest about what is here called “endogenous’ money, which is just a fancy way of saying “the bank makes up money out of thin air.” Meanwhile, in the dumbed-down versions that they write for the consumption of us common folk, they, um…fudge a little bit. Or a lot. Whatever. Long story short, they make you think that banks lend deposits. That’s where you got that idea—that you now know isn’t true, right?

And after all, what’s best kind of mind control? The kind that doesn’t seem like mind control at all. Your kindly old professor “taught” you the textbook version of money creation while the people who wrote the damn textbooks—or who taught the people who wrote the textbooks—knew very well the textbook version was poppycock. After all, there is a “long literature” on the subject—that they wrote. Ah well, it always helps them to get to you early. Get in your mind. Make your mind their enforcer of their untruths. The big lie always seems to work best, as ol’ Adolf put so accurately (and he would know):

“…in the big lie there is always a certain force of credibility; because the broad masses of a nation are always more easily corrupted in the deeper strata of their emotional nature than consciously or voluntarily; and thus in the primitive simplicity of their minds they more readily fall victims to the big lie than the small lie, since they themselves often tell small lies in little matters but would be ashamed to resort to large-scale falsehoods. It would never come into their heads to fabricate colossal untruths, and they would not believe that others could have the impudence to distort the truth so infamously. Even though the facts which prove this to be so may be brought clearly to their minds, they will still doubt and waver and will continue to think that there may be some other explanation. For the grossly impudent lie always leaves traces behind it, even after it has been nailed down, a fact which is known to all expert liars in this world and to all who conspire together in the art of lying. These people know only too well how to use falsehood for the basest purposes. (Mein Kampf, p. 134)”

So the message from the BoE? Don’t be a dupe from all that propaganda we fed you that duped you. I also can’t help but detect a hint of “Oh yeah, sucker—we got you good all this time! You completely fell for it!” And now it’s all “But seriously dude, we were just screwing with you about lending out deposits. That’s always been BS, dude. You mad, bro?”

The very essence of what this blog is all about has been spelled out and confirmed in an article by the Bank of England:

“Commercial banks create money, in the form of bank deposits, by making new loans. When a bank makes a loan, for example to someone taking out a mortgage to buy a house, it does not typically do so by giving them thousands of pounds worth of banknotes. Instead, it credits their bank account with a bank deposit of the size of the mortgage. At that moment, new money is created. For this reason, some economists have referred to bank deposits as ‘fountain pen money’, created at the stroke of bankers’ pens when they approve loans.”

Read that again, especially this part: “When a bank makes a loan, for example to someone taking out a mortgage to buy a house, it does not typically do…

My wife is now in jail on Obstruction and Trespassing on her OWN home. She stood for OCGA 44-11-32 & the fact that the Sheriff DID NOT have a Warrant w/ FiFa for us at Our Home. She stood for Justice and Our Home!!

We even had a home invasion by the SWAT Team. She stood for Justice even with our Pro Bono Attorney, the M&T (Attorney Mr. Thomas Howell from McCalla Raymer) came and testified against her. This was the 25th time we have gone to court on this!! We need to get this out in the public!!! HELP!!!!

Some great articles by Bill Butler at Liberty Law, who knows a thing or two about securitization and foreclosure fraud, as he won one of the first (if not the first) lawsuits over securitization in 1996. Butler has been railroaded by the Minnesota federal judiciary, having been fined (and now suspended) in the neighborhood of $323,000 for presenting what the courts called “frivolous” arguments in foreclosure cases.

Of course, “frivolous” really means “bank-defeating” and so therefore the arguments couldn’t be allowed. You know, “frivolous” argument and reasoning like this:

In the example above, Wells Fargo Bank, N.A, as Trustee of the Series 2004-B Trust, claims to be the sole and exclusive owner of the securitized mortgage. If Wells is in fact the owner, it must have acquired legal title to the loan on or before February 26, 2004. New York law states that transfers to a trust after the closing date of the trust are void. N.Y. Estates, Trusts and Powers Law §§ 7-1.18, 7-2.4. Glaski v. Bank of America, N.A., 218 Cal.Rptr.4th 1079 (2013). See also, Saldivar v. JPMorgan Chase, 2013 WL 2452699 (Bky. SD Tex. 6/5/13) (holding that trustee mortgagee’s position is void if notes and assignments of mortgage not delivered within 90 day of closing of trust); Wells Fargo v. Erobobo, 2013 WL 1831799 (NY Slip Op. 4/29/13) (holding that NY trust law governs securitization and that notes and assignments of mortgage must be physically delivered to trustee within 90 days of closing for trustee to have claim of ownership). The Internal Revenue Code provides for 100 percent tax penalties for transfers to the trust after the closing date. So, if Wells Fargo cannot show physical receipt of the note and mortgage prior to February 26, 2004, its claim to the home is void. Similarly, if the only evidence Wells Fargo has of ownership is a document executed after February 26, 2004, its claim is void. Here is an example of such a document. It is an assignment of mortgage executed on May 26, 2010 (“5/26/10 AOM”) by Mary Kist in Dallas County, Texas. It is patently fraudulent. It was executed six years after the Series 2004-B trust closed. Every fraudulent securitized mortgage foreclosure has this smoking gun. There are millions of these recorded throughout the country.

According to Marie McDonnell of McDonnell Property Analytics, Mary Kist is a robo-signer. Ms. McDonnell’s thorough and pro bono analysis performed for the Essex, Massachusetts Register of Deeds is here. Mary Kist, sitting in Dallas Texas, had no factual knowledge of the contents of the 5/26/10 AOM and no legal authority to sign it. The fact that Wells Fargo had to go to Dallas, Texas to find someone to sign the 5/26/10 AOM when it is headquartered in San Francisco is powerful and dispositive evidence that it did not acquire legal title to the loan prior to February 26, 2004. These fraudulent assignments of mortgage exist in every securitized mortgage foreclosure. They are always executed years after the closing of the securitization trust and typically by someone who has no idea what they are signing. They are also always executed in a state a long distance from, and outside the subpoena power of, the state in which the foreclosed property is located.

The significance of the too late assignment of mortgage is this. Wells Fargo never acquired “legal title” to the securitized loan. This is an unfixable error. It also exposes the MBS holders to 100 percent tax penalties. Because of this, Wells Fargo, according the Erobobo, Salidivar and Glaski cases cited above, does not and cannot have “legal capacity” or legal “standing” to make a claim to the property. In short, the 5/26/10 AOM is irrefutable evidence that the Series 2004-B Trust is a “busted trust” with no identifiable owner of the mortgage.

Of course, not only was Bill Butler fined and suspended–he himself is now a victim of the very foreclosure fraud he is now barred from attempting to stop. So he figures, why not tell you what happened to him. Like me, he was fighting Fannie Mae:

Fannie Mae’s fraud differs from private securitization fraud. Although Fannie Mae is subject to the same trust rules and makes the same representations regarding physical receipt of securitized notes and mortgages prior to the “Issue Date” of the MBS, Fannie typically comes into record title after the foreclosure. In a typical Fannie case in Minnesota, an entity like Bank of America will conduct the foreclosure and then deed the property to Fannie Mae. Attached is a September 7, 2010 quit claim deed (“9/7/10 QCD”) from BAC GP, LLC to Fannie Mae relating to my home. As you can see, the “total consideration” for this transfer was “less than $500.” Jill Landeros, as “Assistant Secretary” of “BAC Home Loans Servicing, LP” executed the deed in New York. The 9/7/10 QCD claims, without any independent authority, that BAC GP, LLC is the “general partner” of BAC Home Loans Servicing, LP.

If this was done properly in accordance with the Fannie Mae Trust Indenture and Custodial Agreement above, Fannie Mae would have taken legal title to this loan in 2006 and would have in its possession the original note and fully executed assignment of mortgage dated sometime in 2006, the loan origination date and prior to the MBS Issue Date. For the same “busted trust” reasons cited above, because the 9/7/10 QCD is dated four years after last possible closing date of this securitization trust, Fannie Mae does not have legal title to this loan. Like the above example, the 9/7/10 QCD is powerful evidence that Fannie Mae never obtained legal title to this loan.

There are other nuances relating to Fannie Mae foreclosures, including the application of District of Columbia trust law and the occasional fraudulent assignment of mortgage to Fannie, but generally the above—bailout bank servicer with no right, title or interest in the loan conducts the fraudulent foreclosure and then deeds its interest to Fannie Mae—is how Fannie Mae illegitimately steals homes.

Now, most judges will downplay all of this and quite readily rule against anyone making these arguments. Even a lot of attorneys will tell you that, while all of this is true, you did borrow money and do owe it to somebody and that the best you can hope to get from arguments like these is delay in the foreclosure process and you risk really raising the ire of the court if you press on with these arguments. Fortunately, there are lots of procedural snafus that can be used against the banks that don’t have to involve the floodgates-opening truth, so a lot of times those get used against the banks with good results.

…and with good reason. You can’t trust these banks! Everybody know this by now. Bank of America is concerned that mortgage applications are down:

“Bank of America Merrill Lynch (BAC) analysts just emailed a research note reminding clients they feel the Fed needs to continue to back the mortgage market if the so-called housing recovery is to remain intact.

Justin Borst and Chris Flanagan say the fundamental numbers behind household formation — mortgage purchase application activity — remains critically weak.”

This is what happens when fraud is the business model, like it is with these banks. Sooner or later, people will learn they can’t trust the banks and other fraudsters. Seems maybe people are finally learning that lesson.

The BoA analysts’ solution to this problem? One might think they’d say that fraud should not be their business model. But of course they don’t. They just want more free money from the Fed to keep the fraud going:

The housing recovery may not continue, they indicate, if the Federal Reserve continues to pull back on its purchase of mortgage-backed securities and decides to raise rates sooner-than-later.

[SNIP]

“Until proven otherwise, these numbers are awful, and create a need for continued Fed accommodation and a positive technical backdrop for securitized products, especially credit,” they add.

The powers that be are trying to convince us that inflation is a good thing, a healthy thing, as Peter Schiff notes here:

“It is no accident that the concept of ‘inflation’ has experienced a dramatic makeover during the past few years. Traditionally, mainstream discussion treated inflation as a pestilence best vanquished by a strong economy and prudent bankers. Now it is widely seen as a pre-condition to economic health. Economists are making this bizarre argument not because it makes any sense, but because they have no other choice.”

I should note that, while there are a number of times I find Schiff hard to take, this is not one of them. He’s exactly right. Inflation is the bane of our existence. It’s the hidden tax (that isn’t really hidden) that decimates the buying power of the average person, i.e., you and me.

Inflation is the bane of our existence because even though prices are inflated–that is, prices increase–there is no discernible or actualincrease in the quality of the goods or services for which we are charged inflated prices. The old saying “You get what you pay for” doesn’t really hold water under such circumstances.

Inflation is of course, also the reason that the dollar has lost virtually all of its purchasing power since 1913. So what is The Financial System doing to keep us from rioting in the streets and surrounding government buildings? They’re faking us out, as Schiff notes:

“We are creating debt now in order to push up prices and create the illusion of prosperity.To do this you must convince people that inflation is a good thing…even while they instinctively prefer low prices to high. But rising asset prices do little to help the underlying economy. That is why we have been stuck in what some economists are calling a ‘jobless recovery.’ The real reason it’s jobless is because it’s not a real recovery! So while the current booms in stocks and condominiums have been gifts to financial speculators and the corporate elite, average Americans can only watch from the sidewalks as the parade passes them by. That’s why sales of Mercedes and Maseratis are setting record highs while Fords and Chevrolets sit on showroom floors. Rising prices to do not create jobs, increase savings or expand production. Instead all we get is debt, which at some point in the future must be repaid.“

However, as Michael Hudson is fond of saying, debt that can’t be repaid won’t be. Except in the case of The Financial System–they will again be bailed out once this new debt/infation bubble pops–their debts will be made good via taxpayer money. As Schiff notes, this is already being done with quantitative easing and ZIRP, while we argue with each other over whether minimum wage should be raised. Short answer–the minimum wage absolutely must be raised as long as this fictional system keeps creating fictional moneywith which to enslave us. And which will be the cause of war after war after war after war in order to prop up this insane system. See Dr. Hudson talk about fictitious capital here with Max Keiser (you simply must watch from approximately 2:00-4:00; sums it all up):