Hat tip to Robert Tuna Townsend (a Facebook friend) for this. Great talking points for shutting down the inevitable “but you didn’t make your payments and just want a free house” argument.

Hat tip to Robert Tuna Townsend (a Facebook friend) for this. Great talking points for shutting down the inevitable “but you didn’t make your payments and just want a free house” argument.

It’s time to end fractional reserve banking and admit that money is fictional. It’s time to cut off the free money supply to the banks and redirect it to we the people.

In the video below, Godfrey Bloom of the UK Independence Party (UKIP) explains the problem with the world economy. For those who may not wish (or don’t have the time) to watch the video, here’s the essence of what Bloom says: the problem with the world economy is that through “fractional reserve banking,” banks are allowed to “lend” “money” they do not actually have. He also points out that “quantitative easing” is in fact, counterfeiting.

In other words, banks are allowed to create and receive FREE MONEY, and that is a SCAM on you and I, hence the name of this post. As I explained in a previous post:

“Simply put, the problem with the U.S. economy is free money. No, money is not free to you and me, it’s free to those who ‘loan’ ‘money,’ like banks and credit card companies. Indeed, it took me a…

View original post 1,094 more words

In the latest smackdown of the big banks making the rounds, namely JP Morgan Chase Bank, Natl. Assn. v Butler, heroic Judge Arthur Schack puts Fannie Mae in her place more than any other judge I’m currently aware of. He takes Fannie to task over a portion of Fannie’s Servicing Guide (Part VIII, Chapter 1, Section 102) that I have always found shockingly arrogant and at odds with the law.

Schack quotes the whole offending section, but I’ll just give the most arrogant parts:

“Fannie Mae is at all times the owner of the mortgage note, whether the note is in our portfolio or whether we own it as trustee for an MBS trust.In addition, Fannie Mae at all times has possession of and is the holder of the mortgage note, except in the limited circumstances expressly described below. [SNIP]

[Schack italicizes the following section] In any jurisdiction in which our servicer must be the holder of the note in order to conduct the foreclosure, we temporarily transfer our possession of the note to our servicer, effective automatically and immediately before commencement of the foreclosure proceeding. When we transfer our possession, our servicer becomes the holder of the note during the foreclosure proceedings. [SNIP]

[Schack also italicizes the following section] This Guide provision may be relied upon by a court to establish that the servicer conducting the foreclosure proceeding has possession, and is the holder, of the note during the foreclosure proceeding, unless the court is otherwise notified by Fannie Mae.”

Schack correctly concludes that “FANNIE MAE’s Servicing Guide, with its deceptive practices to fool courts, does not supercede New York law.” I had the same thought when I first encountered this fiat decree of Fannie Mae’s when researching my own lawsuit against Fannie Mae and others a couple of years ago. It is a relief to hear a judge articulate this so starkly.

However, I am somewhat dismayed to read that Schack refers to Fannie Mae as the “owner” of the note and mortgage throughout his decision. Schack appears to be relying on affidavits from Fannie Mae/Chase types for this information, as he must. I haven’t read the affidavits on which Schack relied, but I have read information from Fannie Mae’s own trust documentation and website that puts the lie to the idea that Fannie Mae owns anything.

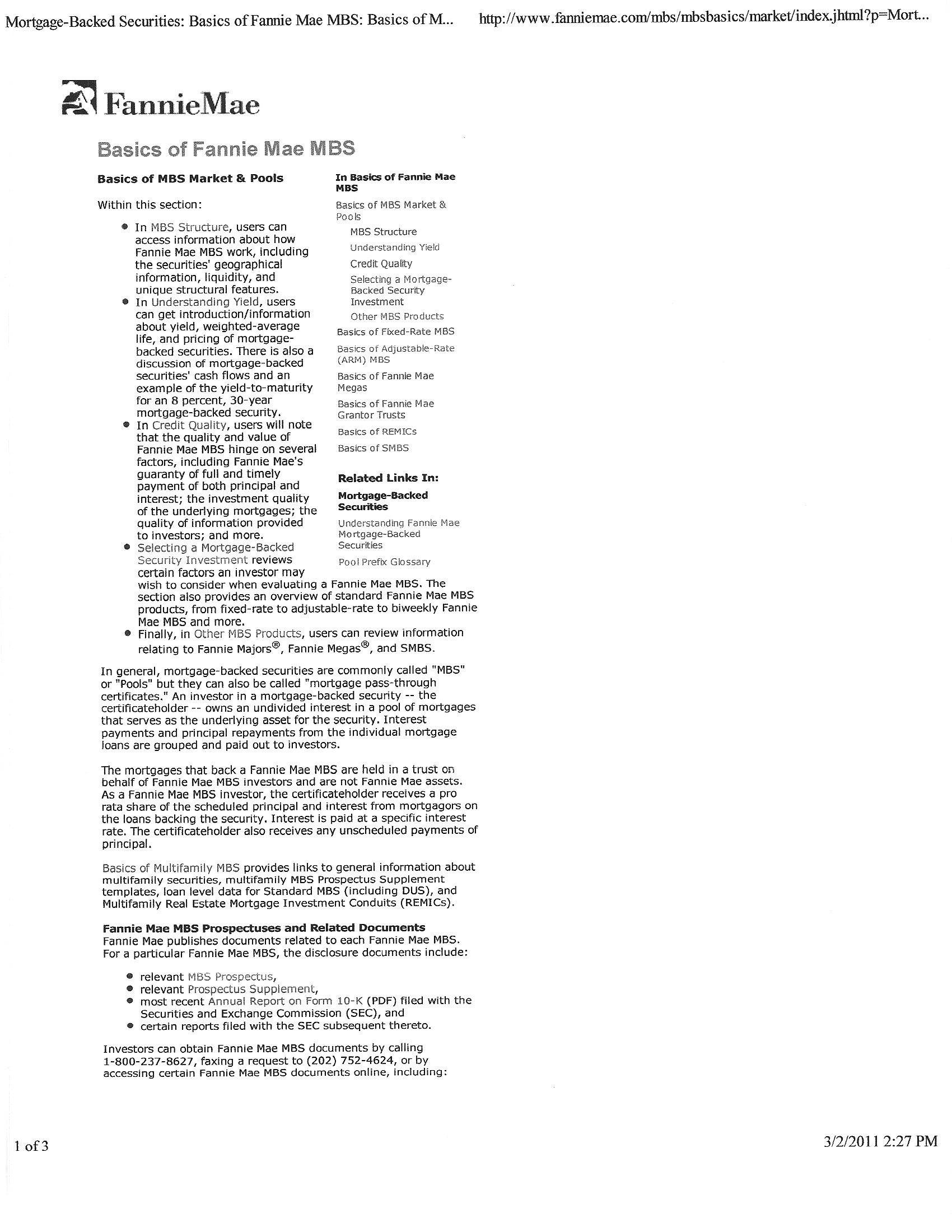

Fannie Mae Tells Us It Owns Nothing

UPDATE 10-8-13! The document referenced in the following sentence used to say what is quoted below. However, reader P Nach pointed out that as of 10-8-13, the document no longer makes that statement, and in fact any Google search with “The mortgages that back a Fannie Mae MBS are held in a trust on behalf of Fannie Mae MBS investors and are not Fannie Mae assets” in quotes brings up practically only this site. Fortunately, back in 2011, I printed out and scanned the page from Fannie’s website that contained this statement. I have uploaded it here and you can view and download it here–any future readers who may find this link removed or not working, please let me know in comments (UPDATE 10-9-13! Reader P Nach submitted a Fannie Mae PDF she found which contains the “not assets” statement on page one–link here: 2012 02 06 Fannie Mae-Basics-of-MBS):

[ORIGINAL SENTENCE AND LINK: A PDF from Fannie Mae’s own website entitled “Basics of Fannie Mae MBS” explains Fannie Mae’s lack of ownership very simply and succinctly:]

“In general, mortgage-backed securities are commonly called “MBS” or “Pools” but they can also be called “mortgage pass-through certificates.” An investor in a mortgage-backed security — the certificateholder — owns an undivided interest in a pool of mortgages that serves as the underlying asset for the security. Interest payments and principal repayments from the individual mortgage loans are grouped and paid out to investors.

The mortgages that back a Fannie Mae MBS are held in a trust on behalf of Fannie Mae MBS investors and are not Fannie Mae assets. As a Fannie Mae MBS investor, the certificateholder receives a pro rata share of the scheduled principal and interest from mortgagors on the loans backing the security. Interest is paid at a specific interest rate. The certificateholder also receives any unscheduled payments of principal.”

So from the above, we see that Fannie itself says that certificateholders–not Fannie–own the beneficial interest in the mortgage pool (Fannie says in other documentation that it can also purchase these types of certificates, although I haven’t seen any indication that Fannie smokes its own dope). Even more importantly, we see that Fannie itself says that the mortgages (i.e., the promissory notes) that are supposedly in the pools/trusts are NOT Fannie assets.

The very definition of the term “asset” of course involves “ownership,” as spelled out at Investopedia’s definition of “asset,” which it defines as:

“A resource with economic value that an individual, corporation or country owns or controls with the expectation that it will provide future benefit.”

Therefore, Fannie admits it neither owns nor controls the promissory notes. So if Fannie Mae itself admits that it does not own the notes and mortgages in the pools, why are Fannie’s goons swearing to Schack that Fannie does own them?

Some people may not be satisfied with such an admission in the text of a website meant to simplify matters. OK, well how about these jewels from the “Fannie Mae Amended and Restated 2007 Single-Family Master Trust Agreement for Guaranteed Mortgage Pass-Through Certificates evidencing undivided beneficial interests in Pools of Residential Mortgage Loans” dated January 1, 2009:

“By delivering at least one Certificate of a Trust in the manner described in Section 3.1, the Issuer [i.e. Fannie Mae] unconditionally, absolutely and irrevocably sets aside, transfers, assigns, sets over and otherwise conveys to the Trustee [i.e., Fannie Mae], on behalf of related Holders, all of the Issuer’s [Fannie Mae] right, title and interest in and to the Mortgage Loans in the related Pool, together with any Pool Proceeds.”

“Concurrently with the Issuer’s [Fannie Mae] setting aside, transferring, assigning, setting over and otherwise conveying Mortgage Loans to the Trustee for a Trust: (a) the Trustee [Fannie Mae]… acknowledges that it holds all of the related Trust Fund in trust for the exclusive benefit of the related Holders [of certificates issued by the Trust]…”

Note that Fannie Mae as Issuer irrevocably transfers all of its interest to Fannie as Trustee, and that Fannie Mae as Trustee says that it holds all the money in the trust for the exclusive benefit of the certificateholders. So again, Fannie Mae admits it doesn’t own notes.

Fannie’s Duplicity–All Things To All People?

Notice the duplicity of Fannie Mae made plain in these documents. In the Fannie Servicing Guide, Fannie’s intended audience is obviously its servicers, so they want the servicers to believe that Fannie Mae is “at all times” both the owner and holder of promissory notes. However, in the other two documents (the “Basics of Fannie Mae MBS” website excerpt and the Amended 2007 Trust Agreement) excerpted above, Fannie’s intended audience is investors and potential investors, both of whom Fannie wants to believe that they (the investors or potential investors)–and not Fannie–are the owners of the promissory notes.

So why is anyone letting Fannie Mae get away with saying that it owns promissory notes (and by extension the deeds of trust/mortgages) and can foreclose due to that ownership? Please spread this info far and wide.

(Judge Nelva Gonzales Ramos)

The judge’s denial of MERS/BoA’s Motion to Dismiss in the case of Nueces County v. MERS et al. is AMAZING! Not because it’s novel, but because it actually follows the law! It’s like Neil Garfield or Matt Weidner or David Rogers wrote it. Or like I wrote it! In fact, in my losing case of Kirby v. Bank of America (Southern District of Mississippi, 2012), I did use many of these same arguments–any sane, reasonable person would have! You have got to read this decision!

Normally I might be tempted to highlight a sentence or two from the judge’s order and then mumble through my understanding of it, but with this brilliant order, all that needs to be done is to provide the blockbuster, bombshell quotes from it (for those who may not have the time or inclination to read it). The quotes themselves are commentary enough, so here goes:

1. “MERS does not, however, hold any beneficial interest in the deeds of trust, and it is not a beneficiary of the deeds of trust. It is merely an agent or nominee of the beneficiary.” (p. 14)

2. “By having itself designated as the “beneficiary under the security instrument” in the deeds of trust presented to the County Clerk for recordation in the County’s property records, knowing that it would be listed as the grantee of the security interest in the property, it appears that MERS asserted a legal right in the properties. The Court concludes that, viewing the FAC’s allegations in the light most favorable to Plaintiff, one could plausibly infer that the recorded deeds of trust [naming MERS as “beneficiary”] constituted fraudulent liens or claims against real property or an interest in real property. “ (p. 14)

3. “While Defendants may not have acted with the actual purpose or motive to cause harm to the County, the FAC alleges that through their creation of MERS, Defendants intended to establish their own recording system in order to avoid having to record transfers or assignments with the County and paying the associated filing fees. (FAC ¶¶ 2, 3, 17.) Accordingly, one can reasonably infer from the allegations set forth in the FAC that Defendants were aware of the harmful effects the fraudulent liens would have on the County. That is sufficient to establish intent.” (p. 16)

4. “Accordingly, the Court concludes that the FAC sets forth sufficient facts to give rise to a plausible inference that Defendants made false statements to the County regarding their rights under the deeds of trust and their relationships to the borrowers in the mortgages issued by MERS members.” (p. 22)

5. “County records as having a security interest in the properties. Accordingly, viewing the allegations of the FAC in the light most favorable to Plaintiff, the Court concludes that one could plausibly infer that Defendants made material misrepresentations of fact to Plaintiff in the deeds of trust presented to the County for filing.” (p. 23)

I’m so excited I can hardly contain myself! This judge gets it EXACTLY right! She even defers to Carpenter v. Longan! There is obviously a major schism in the Texas federal judiciary, and this judge–Nelva Gonzales Ramos (an Obama appointee)–comes down on exactly the right side!

Don’t mess with Texas!

In Nueces County, Texas, MERS will be going to trial because, according to a Bloomberg article:

“The county alleges that properties bundled into mortgage securities may have traded dozens of times within the MERS system without the county being notified of any change in ownership.“

That is the EXACT problem with MERS. Not only is the county notified of change in ownership, the homeowner is not notified of change in ownership. MERS is like a game of musical chairs for banks: while the homeowner’s monthly payments are coming in, the note changes hands multiple times-without the county or homeowner knowing of this hand-changing–and when the music (payments) stops, MERS is always able to find a chair because supposedly MERS can purport to be the nominee/agent of ANY bank. So no bank can ever lose at musical chairs, because MERS is their “ghost man” they can put in whatever chair they need to put him in, even if no bank is an actual creditor and shouldn’t still be playing the game.

MERS is about opacity, not transparency

However, this little scheme is not the point of recording ownership with the county recorder. The point of recording ownership is so that the public–i.e., the county, the homeowner, the courts, any interested party–can always know who really owns what property. The banks of course, do not want this sort of transparency, because if there was such transparency, the whole securitization Ponzi scheme would be revealed for what it is, i.e., a complete con game. So the very business model of MERS certainly goes against the spirit of recording laws, even though it may adhere (however tenuously) to the letter of the law. The judge recognized this:

“‘This court cannot simply bend the laws of Texas to fit the MERS system, no matter how ubiquitous it has become,’ Ramos said. She rejected the bank’s argument that she should ‘turn a blind eye to the fact this process does not comply with the law’ because MERS is involved in 50 percent of the county’s residential mortgages.”

Ah–the cracks are appearing in the “too big too fail” dam that is holding back a reservoir of fraud!

(h/t: STOP Foreclosure Fraud)

Neil Garfield of Living Lies gets it right again about the case of Barbara Bratton, correctly labeling what happened to her “judicial hypocrisy.” As Garfield writes:

“There is something happening here and it is beginning to bother me more and more. A number of people have attempted to file papers in the county recorder’s office in order to preserve their ownership rights to property that is either in foreclosure or has been the subject of a foreclosure sale. As I’ve stated on these pages most foreclosure sales are an illusion. Credit bid is submitted by a non-creditor on behalf of other parties who are also non-creditors.

I might add that many pundits, writers, bloggers and lawyers have actually recommended to clients that they file any legally defensible document in opposition to a change in title or possession that would result from enforcement of fraudulent bank documents that are recorded in the public records. Our view is that the very existence of MERS is proof enough of fraudulent intent by the banks, their attorneys, the trustees on deeds of trust, and the other parties involved in the foreclosure and securitization scheme. Our view, like the oath that every attorney takes before becoming licensed, is that every effort should be made to advocate for the position of someone who is in an adversarial position. This does not include making false statements or recording false documents. But the issue becomes very cloudy when one side is allowed to file false documents and the other side is not.”

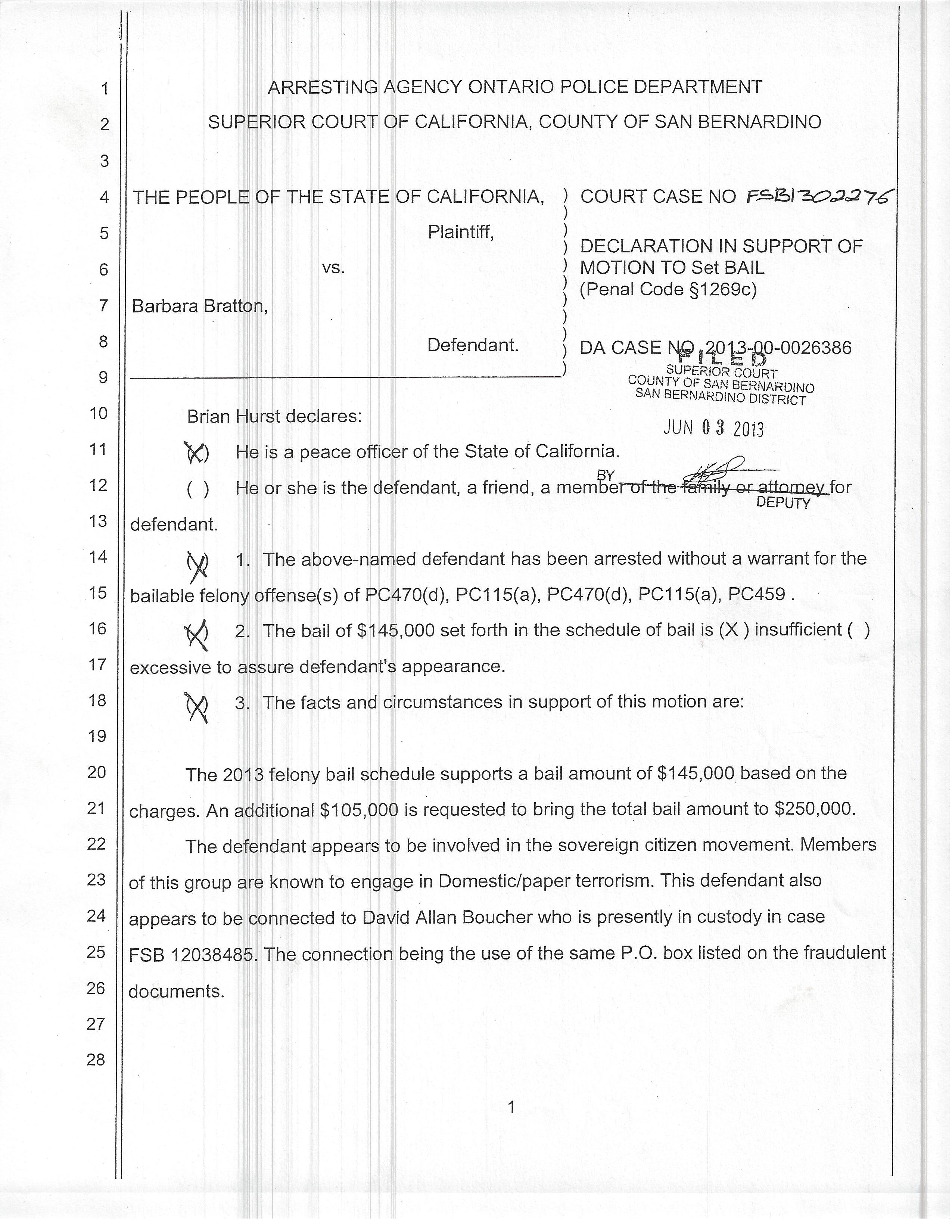

Seriously, “terrorism?”

It would be one thing if the San Bernardino authorities had simply ordered Bratton’s documents expunged from the county recorder’s files. That would be the simple, cheap (for the taxpayers), and easy thing to do. Instead, these “authorities” want to make a federal case–masquerading as a state case–out of it. I say that because apparently there were FBI agents present at Bratton’s bail hearing. What federal law did Bratton violate? She is being charged under California law. Since when does the FBI have anything to do with California law?

But instead of doing the simple, cheap, easy thing, they had to go and try to make Bratton out to be a terrorist, which any sane person knows is completely ludicrous. That is really where the line got crossed. Interestingly, however, Bratton has not been charged with any terror-related offenses. Not yet, anyway. I have a feeling that the more publicity is given to her case and the more awareness of it increases, there may be a gag order issued in her case like there was in the case of Jeff Olson, the San Diego chalk “vandal” (sanity thankfully prevailed in his case and he was completely acquitted yesterday). Or, maybe the complete opposite will happen and the authorities will back off due to public pressure.

Hopefully the second option will prevail–and to that end, here is the ridiculous declaration of Officer Brian Hurst, stating that Bratton is a domestic or paper terrorist (no, the banks are!). To be accurate, the declaration labels Bratton a domestic/paper terrorist because of her alleged association with the sovereign citizen movement, but nonetheless, the damage is done. This is public record and it has been written about, but the actual document has not yet been made available online that I am aware of. So here it is below in all its glory–when you read it, ask yourself whether or not this crosses the line: