NOTE: This interview was conducted in late February 2014, before a sentencing hearing that was eventually postponed. Ms. McCulley was then sentenced to a year each of prison and probation on April 25, 2014. She is now requesting a Reconsideration of her sentence, and this request will be heard on May 8, 2014.

Originally published: May 7, 2014

By Clinton Kirby and Glenn Augenstein

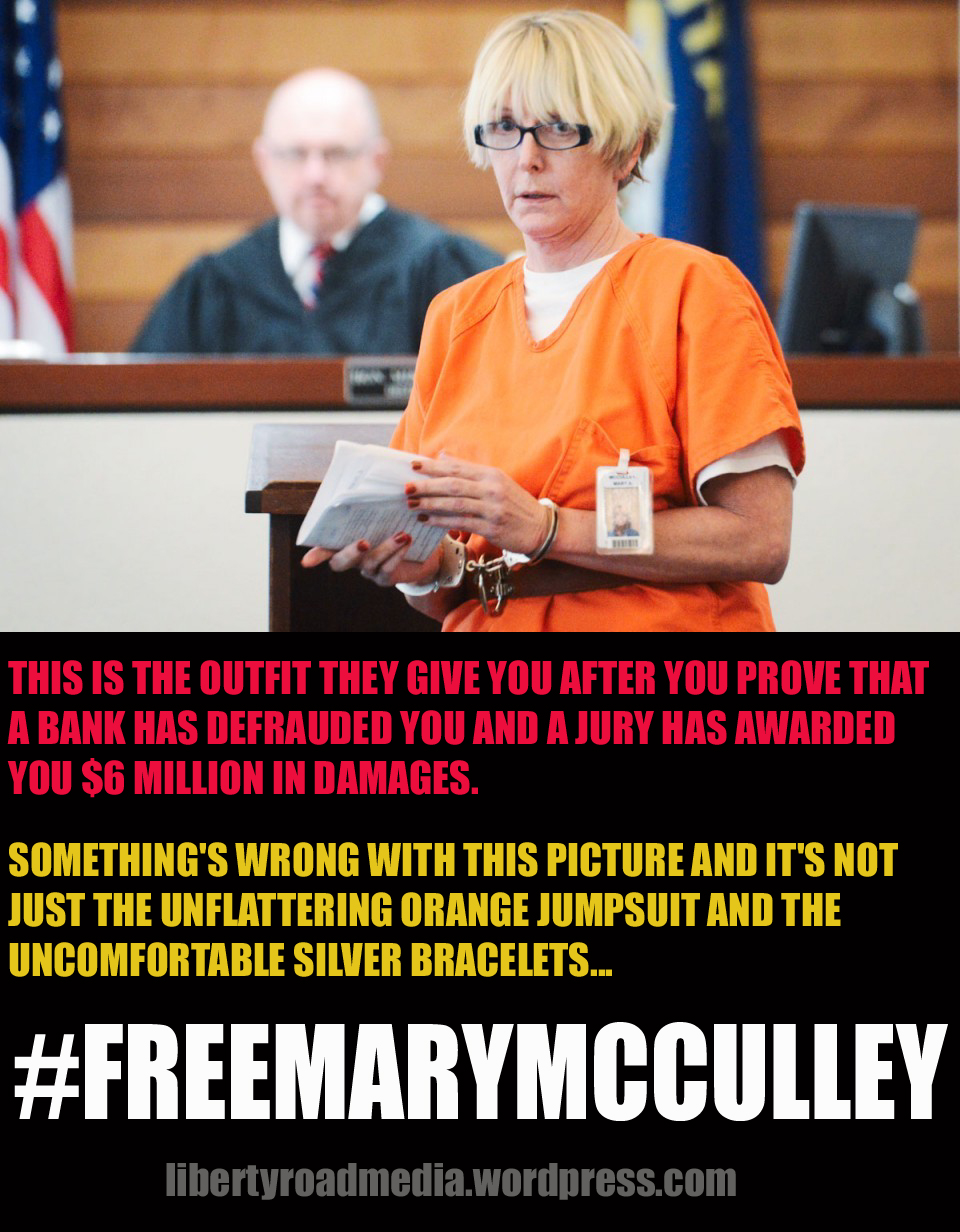

If you follow the news of foreclosure fraud and bad banks, you have certainly heard that on February 7, 2014, a Gallatin County, Montana jury awarded Ms. Mary McCulley an incredible $6 million verdict against US Bank of Montana, with $5 million of that figure being awarded for punitive damages.

It’s the kind of victory that foreclosure fighters have long dreamed of, yet rarely (if ever) seen: a bank being found liable for actual fraud as well as constructive fraud. Indeed, the fact that banks have committed fraud related to foreclosures (among other things) is common knowledge to both the public and the government, but the banks usually get away with it because judges inexplicably let them off the hook in any number of lawsuits (usually performing extraordinary feats of legal gymnastics to do so), or there are undisclosed settlements with homeowners, or the regulators give them a slap on the wrist in the form of either fines (that are proportionally miniscule to the banks’ financial gain from their illegal behavior) or essentially toothless settlements (sometimes both).

So in that context, the jury’s verdict in Ms. McCulley’s case is remarkable to say the least and it provides hope that all is not lost, and that the tide is turning—or has turned—against the banks.

Perseverance and fighting spirit

However, Ms. McCulley’s road to victory was not an easy one. If she had given up the fight at any number of stops along the way, it would have been completely understandable. And the depressing part is that, even though she has this monumental victory under her belt, she is now incarcerated in a Montana correctional facility on what many believe are dubious charges. Those charges apparently stem from complaints filed by Tom Cahill, formerly of American Land Title Company, and Attorney J. Robert Planalp, who made appearances on behalf of American Land Title Company. American Land Title Company, and U.S. Bank of Montana, were named as Defendants in a civil suit brought by Ms. McCulley in June of 2009. That is to say, even though U.S. Bank of Montana was found to have defrauded her, Ms. McCulley is the one doing jail time—not anyone at the bank, or anyone else who may have been involved in the fraud against her.

“By throwing me in jail for investigating my own fraud, when the FBI wouldn’t help me, and to punish me instead of the actual people that did forgeries and stuff, I think that is a very sad statement,” Ms. McCulley said in an interview conducted in late February 2014, shortly after she won the $6 million jury verdict, but before she was sentenced on April 25, 2014. “So that’s what’s kind of keeping me down. There needs to be a happy ending here, and not just for me, but for all of us that are fighting these banks, you know? Millions of us. Millions of us!”

What makes Ms. McCulley such an admirable woman is that she knows we’re all in this together.

Like many people fighting foreclosure, Ms. McCulley first contacted government agencies for help. It was later discovered that prior to recording, the deed of trust to her property had been altered by Tom Cahill (formerly of American Land Title Company) without her knowledge or consent. Among the agencies she contacted was the FBI. “So the sad thing to me is that I had undisputed facts that there was a forgery. And the FBI just [said], you know–‘Have a nice day’–and they shoved me under the bus. And so did pretty much every other government agency that I went to.”

Understandably dissatisfied with the response she received from the government, in June 2009 Ms. McCulley sued American Land Title Company and U.S. Bank of Montana. Her case was heard in District Court of the Eighteenth Judicial District, In and For the County of Gallatin (Cause No. DV-09-562C), Honorable John C. Brown, Presiding Judge. Despite compelling evidence that her deed of trust was altered after she signed it—but before it was recorded with the county—on January 12, 2012, the District Court granted motions for summary judgment in favor of U.S. Bank of Montana and American Land Title Company.

During this time, Ms. McCulley almost gave up. “At my trial with US Bank, it was proven that their actions were so malicious and heinous—they drove me to a suicide attempt. And you know who I wrote my letter to when I was going to kill myself? The judge. I didn’t write it to my mom or my brother—I said, ‘Dear Judge Brown, I quit. They win.’ And went on to explain the fact that the title company’s lying, the bank’s lying, the lawyers are lying—how can I possibly fight this case when officers of the court are going to lie under oath?”

On April 25, 2012, Ms. McCulley was arrested on several charges, including a felony Assault with a Weapon. Ms. McCulley was held on a $1 million bond. At trial the jury passed on all but one of the charges, and came in with a guilty verdict for a misdemeanor assault charge. Ms. McCulley was sentenced to 6 days. After serving 309 days (303 more than the sentence), she was released.

Undeterred, Ms. McCulley did not give up the fight. While incarcerated she contacted a paralegal who agreed to help her write an appeal of her unfavorable court decision, which was eventually heard by the Supreme Court of Montana. “So I’m in jail, and I’m filing the appeal—and you don’t have anything but an ink pen—but I had a pay phone and I found a paralegal, this guy Alex. And he came, and I told him the story and he helped me write it and we got it to the Supreme Court.”

Alex is deserving of some gold stars, and perhaps an adult beverage, or two.

Ms. McCulley was released in early March 2013. On April 9, 2013, the Supreme Court of Montana ruled in Ms. McCulley’s favor, stating in part: “For these reasons, we reverse the District Court’s order of summary judgment in favor of the Bank on the issue of fraud and remand the matter to the District Court for further proceedings.” American Land Title Company was dismissed from the suit, but U.S. Bank of Montana was not.

Upon remand, and through the trial of February 7, 2014, the jury recognized the defendant had been, to put it mildly, considerably less than honest and forthcoming. Judge Brown, in his April 14, 2014 “Findings of Fact, Conclusions of Law and Order re: Punitive Damages,” said:

At page 10, par. 37, “The Bank made these false statements to the Court in 2011, and the Court relied on the false statements in its summary judgment order.”

At page 13, par. 7, “When, as here, there is concealment of evidence of improper motive the Court will consider this in assessing reprehensibility of the Bank’s conduct.”

At page 13, par. 8, “Further, US Bank ‘blatantly misrepresented an important fact’ in one of its briefs filed with this Court.”

In the same par. 8, “This egregious behavior by the Bank constitutes intentional deceit and supports the conclusion that the Bank’s conduct was reprehensible.”

In a 1913 Harper’s Weekly article Louis D. Brandeis said, “Sunlight is said to be the best of disinfectants.” Clearly Honorable Judge Brown is in agreement.

Perseverance pays off

“I’ve always kind of known I would win the suit against the bank because of the documents,” Ms. McCulley said. “Like I said, it’s a document case; it’s not a hearsay case. The documents speak for themselves.” The Gallatin County jury agreed, in a big way. “That was a complete—just bombshell dropped. That’s a huge verdict for Montana,” Ms. McCulley said. “I think the money shows that banks can be evil, to get those kind of punitive damages, you know?”

Despite the ordeal she has already endured–and will continue to endure unless she is (hopefully) released from prison in the next couple of days–Ms. McCulley is keenly aware of what her victory means and the potential impact it could have: “I don’t know if I’ll ever see a dime. But I want this to be something that somebody else can use. Or that we could parlay into some kind of political—something, you know–‘Hey wake up! The banks do lie, cheat, and steal. That’s the whole goal, you know.”

Ms. McCulley is currently incarcerated in the Cascade County Correctional Facility, Great Falls, MT. Her reconsideration hearing is scheduled for tomorrow—Thursday, May 8 at 3:00 MDT.

To contact the reporters on this story:

Clinton Kirby: leftbehindchild@gmail.com, Glenn Augenstein: mrgl7enn@yahoo.com

#FREEMARYMCCULLEY