You know that cold dread that drops into the pit of your stomach when you check your balance and see that you’re down to your last few dollars and payday is still a week away? Too much month at the end of the money? Of course you do–we all do.

You know that cold dread that drops into the pit of your stomach when you check your balance and see that you’re down to your last few dollars and payday is still a week away? Too much month at the end of the money? Of course you do–we all do.

And what thoughts go through your head when this happens? “I gotta get more hours,” or “I gotta buy the off-brand peanut butter from now on,” or “I am a worthless piece of shit that can’t provide for myself/my family.” In short, you think there’s something wrong with you–something you’re not doing right. That you’re some kind of profligate money-waster even though you’re wearing secondhand clothes sitting on a Goodwill couch in your rented house in the questionable neighborhood with your near-decade-old used car in the driveway–so you gotta cut back.

You must deny yourself–that trip to the movies, that shirt that’s on sale but you don’t really need, the creamy Jif (which although the generic brands taste more or less the same, they just don’t have the same…creaminess), etc. You’re working, sure–two jobs. It was the best you could do after the layoffs. You’re working longer and don’t make anywhere near what you were making before, but hey–at least you’re working. Still though, your credit score is trashed and you had to cut up the cards a while back.

But then you realize–it doesn’t matter that you’re working. You know the cultural imperative: you must impose austerity upon yourself. The money just ain’t there.

It’s not you

But you should know that it really isn’t you. It isn’t something you’re doing wrong that makes your wages vaporize quicker than a banker will run to the government for a bailout. From Zero Hedge:

…as reported moments ago by the BLS, real average hourly earnings just posted their third sequential decline in a row, dropping from $10.33 in February, to $10.32 in March, to $10.30 in April, to $10.28 in May.

The article also correctly states that:

…nominal wages are meaningless in a world in which food and energy prices are soaring, and where, as even the BLS admitted earlier, food prices have surged the most since 2011. In other words, what matters are real, not nominal wages.

Real wages are, of course, the actual buying power of one’s wage, i.e., the inflation-adjusted wage number. The nominal wage, of course, is the number your employer tells you you’re making. And that number is meaningless–if you make $100/day but a loaf of bread costs $200, you’re not making that much money.

The Zero Hedge article makes one other salient point:

And to put today’s $10.28 real average hourly earnings number in context, this is the same real wage seen last in July 2013, July 2012, March 2011 and then, if one goes further back… the month after Lehman failed!

Which, as you’ll recall, was in 2008–6 years ago. But wait, here’s the punchline:

In other words, while the S&P has nearly tripled since its lows real American wages are…. unchanged.

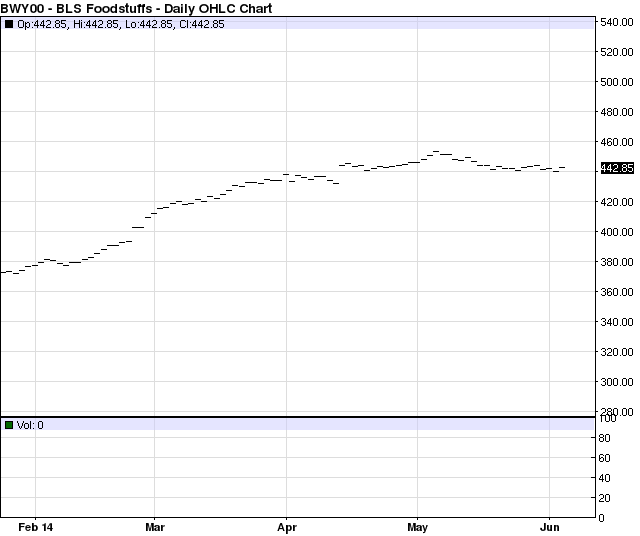

That is to say, the S & P 500 hit a low of 683.38 in 2009 (after a steady tumble throughout 2008) and is now at 1924.97–the almost-tripling referred to above. Meanwhile the real purchasing power of your wages is back to 2008 levels. Here’s the chart from StockCharts.com:

From Free Chart section of StockChart.com; used without permission

Consolation is good, action is better

Hopefully this information comes as some kind of consolation. But hopefully it is also infuriating enough to inspire action. What kind of action? Not sure, to be honest with you. Could start by educating others, conveying this information to them–that hard work and constant hours spent on the job are not the answer to their personal economic problems or the economic problems of the country as a whole. That’s something we can all do. Stop buying the bullshit. Stop believing that we must impose austerity on ourselves while our “betters” buy up everything that doesn’t have our name on it and then steal the rest through fraud. And then tell us it’s our fault that we don’t have anything and that if we only weren’t so lazy, unproductive, and unskilled, the world would be our oyster.

Yeah, undoing each other’s mind control would be a great start. Realizing that we have to stop chasing the carrot because the carrot has turned into the stick. We have to remember what’s really important–family, friends, health, freedom. All of these ideas were spelled out very well by “joe2” in the comments section of an article I read recently (presented in its entirety):

I’m not. I lost that obsession and drive to become “wealthy” back in 2000. First, Greenspan crashed the economy. I warned my co-workers he was going to crash it, took out my 401k money, and they all ridiculed my and said I was crazy. Six months later they lost over half of their retirement accounts. I lost nothing – at the time.

So I buy a home in Atlanta, where I worked. Mistake. But you know, the wife wants a house. I made $84k a year at the time working for a major telecom equipment company. I lived like a king. I never had to worry about not paying a bill or not having a pile of cash in the bank. My wife did not work. 6 months after I bought the house the whole house of cards came tumbling down.

Then, on the eighth and final round of layoffs, my group got the axe. By the time it was said and done, 50,000 people in that company lost their jobs. Stock went from $90 share to $4. Ok, I thought, I’ve been through two layoffs, and found work within 3 months. I’ll pull through this. Nope. Two months later the government pulls 9/11. My fate was sealed. Things have never been the same. It took me 5 years to begin to recover. I could not find work anywhere doing anything. If you had a degree then nobody would hire you. They thought you’d leave as soon a good tech job opened.

So I lied about my whole resume and work experience, and then immediately got offered a job. Instead, I worked at the University for a pittance, but got my tuition paid for, insurance, and got a M.Sc. degree. That allowed me to get back into real work. But it took me several years to get back to $84k/year. Now I’m at 96k, but that money goes half as far as it did in 2000. I was upper middle class. Now I’m what they’d call middle class, but not really, as it’s been redefined in my opinion.

I should be living quite well, but I am not. That money, with a family, now goes nowhere. Sounds like a lot to a lot of people, but it is NOT. The cost of living is so high now that I live half as good as I did, and basically live paycheck to paycheck. I don’t have a 4000 sq. ft. house like I did before. I don’t have a $50k 3000GT twin turbo and a Toyota Sequoia in my driveway like I did before. I don’t have the expensive hobbies I had before. I don’t have money stashed in the bank. Taxes and inflation have turned my $96k into the equivalent of about $30k back in 2000 and that is not an exaggeration.

Now, they are ready to implode it all again, after already imploding it in 2008. Each time gets a little closer. Now it is 2014, six years since the last engineered crash, and it appears overdue and inevitable. I predicted the crash in 2000, 2008, and now I’m telling you it is time again. So I don’t put much effort into achieving wealth because it just simply cannot be attained legally for the average American. The dream is dead.

I’ve learned health, family, love, kindness, and the free things in life are what it is important and brings happiness. Striving in the rat-race to become “rich” will not bring satisfaction or happiness and it is no longer attainable. I fully expect to be right back to where I was in 2000 again.

But this time, it won’t be over 1,000,000 like it was in my industry who lost it all, it’s going to be far worse. It’s going to be the majority of the population, and when that happens, and after people have rebuilt their lives over and over at the hands of TPTB and the bankers, we will have had enough. Chaos is about to reign supreme.

What? Now I’ll have to finish my Ph.D. so I can find a job when they engineer this coming collapse? Will my pay go down to $60k after that with inflation eating up another 40% of my buying power? Yep, that’s exactly what I expect to happen. So I’m not wasting my time in the rat-race trying to keep up with the Jones’ next door. There is no point in trying to attain wealth as they are not going to allow it unless you are inside their clique or serve them in some way.

There is a great divide, and great disparity in the rich and the average American and that gap gets wider every day. Don’t expect to do anything but “get by” and don’t expect to be able to do that in the coming several years. In fact, I’d expect martial law, chaos, and blood in the streets. As Gerald Celente says, “when people have nothing left to lose, they lose it,” and TPTB thinks they can just keep screwing hard-working people and draining off their wealth with no consequences.

The consequences are coming and they’ve over-played their hand. They have no idea what they are up against when they piss off this nation full of gun toting and angry people. It’s baffling that they think they can take us on, but they damn well are preparing to do just that. Mark my words. Try to enjoy the free things in life, what is left, and look to the important things in life, and stop chasing money and the “dream”. The dream is just that, it is just a dream and cannot be attained now, if it ever could be anyway.