“It” being the stock market, stocks, money, everything, as Matthew McConaughey’s coked-up stockbroker explains in the above scene from “Wolf of Wall Street.”

The important point about it all? “It’s not fucking real,” as McConaughey’s character points out. In other words, they know. The brokers, the dealers, the SEC, everyone. They. Know. They know it’s all, as the McConaughey character says, a convoluted game of illusion with the purpose being to take money out of our pockets and put it into their pockets.

As McConaughey’s character says: “We don’t create shit. We don’t build anything.” Exactly–they steal.

The movie came across to me as more or less a celebration of Wall Street fakery and fraud, but there are a few scenes in it–like this one–that tell us, right there on the big screen, what is really going on…

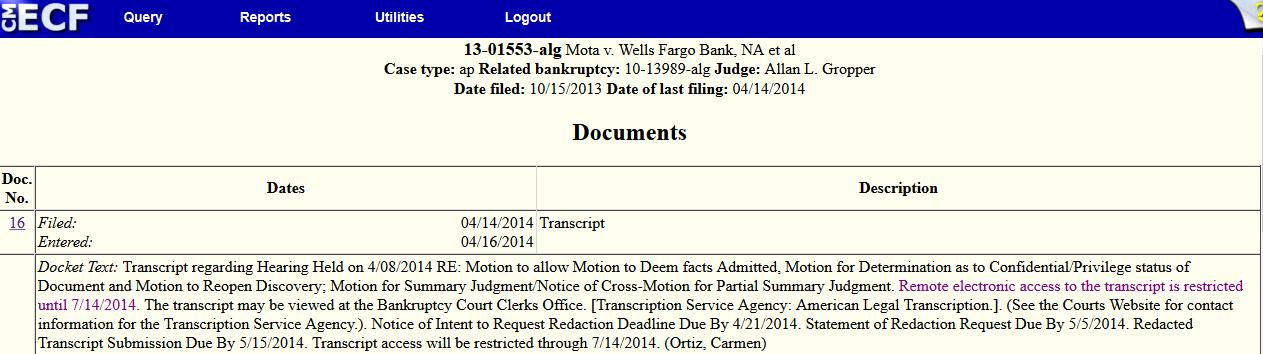

Soon we will have a new deposition to pore and obsess over, getting ever closer to that sweet day when all of this foreclosure fraud is out in the open! Housing Wire explains:

“A New York judge ruled that Wells Fargo (WFC) can’t keep its Home Mortgage Foreclosure Attorney Procedure Manual out of a lawsuit in federal court.

U.S. Judge Allan Gropper agreed to allow the 150-page manual – a copy of which was obtained by plaintiff’s attorney – into a lawsuit being brought on behalf of a homeowner by attorney Linda Tirelli against Wells Fargo, the largest mortgage servicer in the United States.

The case is an objection to foreclosure claims in bankruptcy in Mota v. Wells Fargo.

[SNIP]

As part of the judge’s ruling, Wells Fargo must also provide Tirelli a witness to answer questions about the guidebook in a deposition.”

Granted, the defendants in this case did not oppose the now-infamous Wells Fargo Foreclosure Attorney Procedures Manual being deemed “non-confidential” in their Memorandum of Law filed 4/3/14. They did, however, object to discovery being reopened. Judge Gropper denied that–gotta love it when banks lose motions!

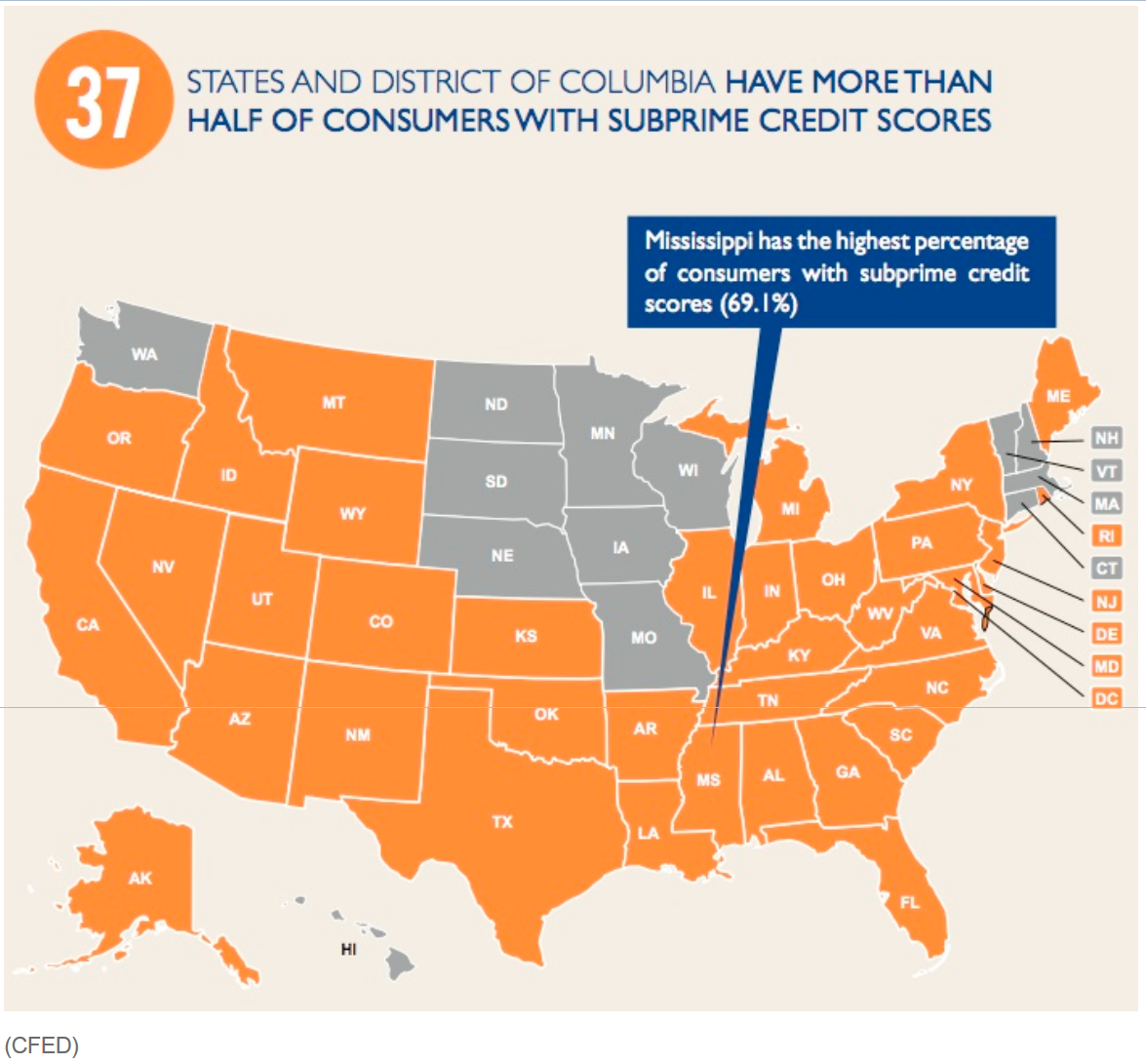

And that’s the point of all these bubbles, and QE, and ZIRP, and inflation– it forces you to finance what you could once buy outright through working. This is the true end game of the “Nixon Shock,” petrodollar, credit bubbles, etc. This is the result of 1971, only 42 years ago. Since then, inflation has gone through the roof, while incomes have stagnated and/or barely kept up with inflation for all but the smallest percentage of Americans. It’s why, as we like to harp on here–in 37 states, over half of consumers have “subprime credit.” That’s what you get when the following happens, as reported by Zero Hedge:

“‘It’s impossible to work your way through college nowadays’…is the hard-to-swallow (but not entirely surprising) conclusion of Randal Olson’s research into just how extreme national tuition costs have become in the US. As The Atlantic notes, the economic cards are stacked such that today’s average college student, without support from financial aid and family resources, would need to complete at least 48 hours of minimum-wage work a week to pay for his courses.”

Randall Olson’s research was based on the cost of tuition at Michigan State (MSU), and concluded the following:

“What we see is a startling trend: Modern students have to work as much as 6x longer to pay for college than 30 years ago. Given the reports that a growing number of college students are working minimum wage jobs, this spells serious trouble for any student who hopes to work their way through college without any additional support.

Let’s crunch a few more numbers to see what a typical year would look like for a student in 1979 and 2013 working her way through college. Most students take 12 credit hours per semester and only attend Fall and Spring semester. That’s 24 credit hours per year.

The 1979 student would have to work about 10 weeks at a part-time job (~203 hours) — basically, they could pay for tuition just by working part-time over the Summer. In contrast, the 2013 student would have to work for 35 ½ weeks (~1420 hours) — over half the year — at a full-time job to pay for the same number of credit hours. If you’ve ever attended college full-time, you know that this is basically impossible.”

Now, this post is meant to highlight what is but one–albeit a particularly egregious–by-product of financialization that has consumed the productive economy and brought the non-productive economy, i.e., banks, to the fore. Indeed, note Olson’s baseline date–1979, not yet a decade after Nixon closed the gold window.

As Olson notes, it’s difficult to pay for college with unless you work full-time and go to school full-time, which is impossible. It’s impossible because if one went to college from say, 8-noon Mon.-Fri. and then worked 1 p.m.-9 p.m. Mon.-Fri., when does one do one’s papers or read one’s books? Well, the 3-4 hour window between going to bed at midnight or 1 a.m., some wags might say. That 3-4 hour window, of course, has to be shared with other necessary tasks, such as traveling back home from the work place, eating, washing clothes, cleaning house, showering, etc.

At any rate, the point is not really about college–it’s about things that used to be affordable are not any more, and that’s they way The Financial System likes it–the more non-dischargeable student loans, the better!

In a bombshell story about Ginnie Mae and Bank of America–which is a big deal unto itself–Yves Smith brings in the following about MERS (Mortgage Electronic Registration Systems), which is the cornerstone of the securitization fail (Smith quotes Bloomberg):

“As the rest of the housing industry recovers, a little-known firm with a key role in U.S. mortgage finance remains stuck in limbo, wrestling with regulators, lawsuits and the departures of senior employees.

The turbulence feeds uncertainty about the fate of Mortgage Electronic Registrations Systems Inc., or MERS, which documents the ownership and resale of about half of U.S. home loans. A breakdown could force clients such as Fannie Mae (FNMA) and Bank of America Corp. to make costly changes to their loan businesses.

Management hasn’t completed fixes promised in a broad 2011 U.S. settlement designed to stop foreclosure abuses, according to two people briefed on MERS’ operations. Regulators rejected one of the firm’s consultants as unqualified and are examining why four employees hired to help with reforms — including the chief legal officer — recently quit, said the people, speaking on condition of anonymity because the matter is private.

The closely held Reston, Virginia-based firm, a unit of Merscorp Holdings Inc., is also facing scores of lawsuits and state probes that challenge its business model as well as the legality of its filings in hundreds of county courthouses.“

So apparently the cover-up…er, settlement is not proving to be the cure-all for the very real problem of what both MERS and “securitization” really are, i.e. elaborate illusions, grandiose delusions, sound and fury signifying nothing, fakery, flim-flam, bamboozlement. You get the picture.

Apparently Bank of America and Fannie Mae are finally having to admit what they have been denied in lawsuits across the country, i.e., that MERS is bullshit (again Smith quoting Bloomberg):

“’If the use of MERS is found not to be valid, we could be obligated to cure certain defects or in some circumstances be subject to additional costs and expenses,’” Bank of America reported in a February filing. ‘Our use of MERS as nominee for the mortgage may also create reputational risks for us.’

Fannie Mae, in its annual financial report filed in February, also noted the potential effects if the lawsuits or regulatory pressures force changes in MERS.

‘A large portion of the loans we own or guarantee are registered in MERS’s name and the related servicing rights are tracked in the MERS System,’ Fannie Mae’s report said, adding that if the firm couldn’t function in the same way, lenders could be forced to go back to time-consuming and expensive methods of recording land transfers.”

What’s interesting is that none of this has been secret, nor has it been especially hard to figure out. Nor is any of this real. It’s all completely fake.

For example, in the quote above, Fannie Mae says it “owns” loans. No it doesn’t–Kemp v. Countrywidedemonstrated that. Indeed, Fannie was Countrywide’s biggest buyer (and Countrywide was the biggest originator) until they both essentially went bust, and in Kemp, Countrywide employee Linda DeMartini openly admitted that in the regular course of business, Countrywide didn’t endorse notes unless an endorsement was needed to fool a judge in a lawsuit. Indeed, she said she had never seen a note with an endorsement at the bottom! Abigail Field corroborated that by examining notes from New York–Countrywide notes lacked endorsements. And legally, no endorsement means no negotiation, and no negotiation means that Fannie Mae doesn’t own anything.

Furthermore, as I’ve written in these pages before, MERS admitted in my own lawsuit that MERS never owned my mortgage note, that if MERS assignments transfer anything, all they transfer is something that I would argue doesn’t even exist (i.e., “title to” a deed of trust or mortgage), and that even if they do that, that doesn’t transfer ownership of the note, which is the fundamental thing. And who swore to that? William Hultman, one of the head guys at MERS.

Here’s where all this was admitted:

Happy Easter, everybody! Except the banks, of course…

IMPORTANT NOTE/DISCLAIMER: The above article is not legal advice and was not written by an attorney. It is merely a collection of common-sense, rational observations written by a sane, rational layperson with common sense. It is recommended that you consult with an attorney for any and all legal advice and/or action.

Let’s say you are homeless. And broke. And sick. And without electrical power. And a U.S. citizen. Do you think the U.S. government would deliver medical supplies, water purification systems and a generator to you? They would if you were Ukrainian military:

“Hagel, speaking at a press conference at the Pentagon with his Polish counterpart, said the approved aid would include medical supplies, helmets, sleeping mats, water purification units, hand-fuel pumps and small power generators.

‘The United States continues to stand with Ukraine. And earlier this morning, I called Ukraine’s acting defense minister to tell him that President Obama has approved additional non-lethal military assistance for health and welfare items and other supplies,‘ Hagel said.”

However, if you’re United States military and need assistance, guess what? Fuck you, that’s what:

“CNN reported that members of the military redeemed nearly $104 million in food stamps at commissaries in the fiscal year that ended September 30. The Defense Department budget would cut subsidies that service members use to pay for diapers for their kids and to put bread on the table.”

“The Veterans Administration Wednesday responded to questions about why the federal agency was foreclosing on a local army veteran’s home. The letter arrived about 24 hours after the Natasha Taylor and her children were kicked to the curb.

[SNIP]

Tuesday, after constable deputies served eviction papers, workers with a moving company pulled furniture and clothing out of the house. Several members of the work crew even snapped pictures of themselves. It was a final slap in the face in a long ordeal for a former Army Staff Sargent who was almost killed by a roadside bomb during her first tour of duty.

‘That was more humiliating than my things being on my property,’ said Taylor

Taylor’s attorney Stephen Casey says he plans to file a complaint against the VA and the sub-contractor that hired the moving crew. Casey is also filing a complaint with the Constables Office for how they acted when they first arrived at the house.

Attempts to put the Tuesday eviction on hold failed despite a formal inquiry by Congressman Michael McCaul. The response arrived Wednesday and was also sent to Casey.

‘There was nothing they were going to do to let her stay in her home,’ said Casey.

The letter is mostly a rehash of the process. Taylor’s financial problems when she was medically discharged after she broke her back in a car accident. A paperwork backlog with the VA held up her benefits.”

And if you’re a civilian and homeless? Fuck off and die:

“Just a couple miles from where lawmakers set the course on everything from taxes to the availability of housing vouchers for low-income Americans, two homeless people were found dead Wednesday morning, with hypothermia being cited as the likely cause.”

The clear lesson? If you want the U.S. government to help you, join the Ukrainian military.

“Last week, something remarkable happened. The Bank of England let the cat out of the bag. In a paper called “Money Creation in the Modern Economy”, co-authored by three economists from the Bank’s Monetary Analysis Directorate, they stated outright that most common assumptions of how banking works are simply wrong, and that the kind of populist, heterodox positions more ordinarily associated with groups such as Occupy Wall Street are correct. In doing so, they have effectively thrown the entire theoretical basis for austerity out of the window.“

It certainly is remarkable that the BoE would come out with this information at this time. This press release/paper is often characterized as “an admission,” but the thing is, this is not new information. It’s never been a secret or been hidden. It just hasn’t been taught in school. In fact, as discussed here, the BoE admits quite openly that there is a “long literature” on the fact that money is created out of thin air and that school textbooks which say it isn’t are incorrect.

And this is what I was trying to get at in my earlier post, titled “Bank Says: If You Believe Banks Lend Deposits, You Are Wrong.” We have been purposely misled about money creation. We have been purposely trained to think that banks lend deposits and/or the bank’s own, pre-existing money and that therefore we have a duty and–their favorite word–an “obligation” to pay it back. It is this mistaken belief that has caused the financial crisis and this belief that threatens to drag the United States, if not the entire world, into financial ruin.

The truth will set you free

Let me be very clear about what I mean by this. We have been trained and shamed into thinking that we must labor in order to “pay back” money that did not exist until we asked to borrow it (and even then doesn’t really exist except as binary code). As Graeber correctly notes:

“There’s really no limit on how much banks could create, provided they can find someone willing to borrow it.”

The only problem with that statement is Graeber uses the same incorrect term the banks do: “borrow.” Indeed, it’s difficult to discuss all of this properly because the very language required to describe it has become so perverted. That is, what we have been trained to call a “loan,” the bank calls a “deposit.” In reality, that type of transaction is neither of those things.

A REAL Loan vs. a bank “loan”

That is, when you go to your local bank and get a “loan,” your local bank is allowed to enter a few keystrokes into a computer and then pretend that it has lent you money–and expects you to pretend that you have borrowed it. The bank does not have the amount you want to “borrow” sitting in its vault–they literally “make” money (by typing it into a computer) off of your request to “borrow” it.

In reality, you have borrowed nothing and the bank has lent nothing but we all are forced to pretend that a real loan has been made.

An example of a real loan would be if I had a bike and my friend wanted to borrow it. For my friend to be able to borrow my bike, my bike has to exist in the physical world before I can loan my bike to my friend. My friend cannot come to me and ask to borrow my bike, then I type into a computer and the bike suddenly exists.

No, I do not have nor can I create unlimited phantom bikes, I only have the one. And when I loan my friend my one bike that actually existed in the physical world prior to his asking to borrow it from me, I no longer have the bike and cannot use my bike until my friend returns it. I have taken a real risk that my bike may not be returned to me. That is an example of a real loan, and that is how we have been taught to believe banking works, i.e, that banks take in deposits and then people come in and borrow those deposits of pre-existing money that the bank will have to do without until it is repaid and that there is risk for the bank in doing this.

The Bank of England has now told us in no uncertain terms that this is incorrect and is in fact a “common misconception.” The BoE is essentially telling us that banks have taken the common, correct understanding of the words “loan” and “borrow”–that we think of in terms of loaning a bike to a friend in the above example–and subverted and distorted their meaning for the express purpose of making us misunderstand what is actually happening.

Cookies vs. Crackers

Creative Commons – Attribution (CC BY 3.0) Cookie designed by Chance Smith from the Noun Project

It’s similar to when I was a young child and my mother told my sister and me that saltine crackers were cookies. She knew that cookies are not good for you but that our friends would talk about cookies and how delicious they were, etc. and that we would want cookies. She also knew that if we knew what cookies really were, we’d demand to have real cookies, and she wanted us to eat right and didn’t want to have to fight us on that.

So she tricked us, and we thought we were getting a delicious dessert food when in fact we were getting saltines. It’s the same thing with banks and “loans”–we are told that banks are “loaning” us money when in fact they aren’t loaning us anything at all. And just like my sister and I eventually discovered my mother’s well-meaning deception, the Bank of England has now plainly revealed the purposeful deception of the banking system.

But we’re getting off track here, so let me get to the point of how this stuff is the true cause of the financial crisis and the foreclosure fraud and all of it. We could be done with it all if we’d just listen to the BoE which is admitting to us that the money isn’t real. It is up to us to extrapolate the rest, which is this: since the money isn’t real, then the debt isn’t either. Indeed, If we all would accept the truth that the money that was “loaned” to us for houses, cars, educations, etc. was not in fact a loan at all but instead was a purposeful hoax–a trick played on us to get us to spend our lives in a perpetual state of anxiety, panic, and labor that benefits the corporation/state instead of ourselves–we could easily allow all of this “debt” to be forgiven/repudiated immediately and start over from scratch with a new and better system. Indeed, that’s the real story of the Bank of England’s press release about money creation: they are telling us in no uncertain terms that we’ve been had and that we were purposely misled.

One final attempt at an analogy: it’s as though we’ve been in a 2-player video game all this time, with the banks as Player 1 and society as Player 2. The banks have been given the cheat code to get unlimited lives in the game but society has not. The banks can therefore play forever without worrying about being killed in the game, which allows them to always get the high score and never worry about navigating the riskiest levels–because the banks are not taking any risks. They are playing the game risk-free; society is taking all the risks while the banks are getting all the rewards, i.e., power-ups and high scores. So the Bank of England has now openly told us this–they’ve had the cheat code–i.e., free money–and that the idea that banks are taking any risks by “loaning” money is completely absurd and incorrect.

If we would only accept and act upon these truths, we would indeed be set free…

Just a reminder on this lovely tax day that in 1984, the report of the Grace Commission made this statement:

“With two thirds of everyone’s personal income taxes wasted or not collected, 100 percent of what is collected is absorbed solely by interest on the federal debt and by federal government contributions to transfer payments. In other words, all individual income tax revenues are gone before one nickel is spent on the services [that] taxpayers expect from their government.”

Just because you’re paranoid doesn’t mean they’re not after you…

From the “So Absurd It Has To Be Real Department” comes the Drone Survival Guide. I’m gonna keep mine on my phone because when you see one of these, it very well could mean one of two things: 1) you’re being targeted for immediate termination with extreme prejudice or 2) you’re being surveilled for the purpose of indefinitely detaining you (and/or someone you are with)…and/or eventual termination with extreme prejudice. Good times!

As you may or may not know, The Washington Post and The Guardian recently won a Pulitzer for their role in releasing the Edward Snowden documents, a number of which dealt with drones.

Check out the site–Drone Survival Guide–for download in your language. Some useful info from the English version–apparently it is not impossible to hide from drones:

Day camouflage: Hide in the shadows of buildings or trees. Use thick forests as natural camouflage or use camouflage nets.

Night camouflage: Hide inside buildings or under protection of trees or foliage. Do not use flashlights or vehicle spot lights, even at long distances. Drones can easily spot these during night missions.

Heat camouflage: Emergency blankets (so-called space blankets) made of Mylar can block infrared rays. Wearing a space blanket as a poncho at night will hide your heat signature from infrared detection. Also in summer when the temperature is between 36°C and 40°C, infrared cameras cannot distinguish between body and its surroundings.

Wait for bad weather. Drones cannot operate in high winds, smoke, rainstorms, or heavy weather conditions.

No wireless communication. Using mobile phones or GPS-based communication will compromise your location.

Spreading reflective pieces of glass or mirrored material on a car on a roof will confuse the drone’s camera.

Decoys. Use mannequins or human-sized dolls to mislead the drone’s reconnaissance.

The guide I have provided above is useful mainly for identifying shapes of drones you see from the ground, not for reading the names of the drones. Apparently a legible copy of the poster will set you back 10 euro at the Drone Survival Guide site. And in case you doubt the advice given above from the Survival Guide, particularly regarding mobile phones, rest assured that it’s no joke, as Glenn Greenwald (who was responsible for much of the above-mentioned Pulitzer-winning reporting on the Snowden documents) and Jeremy Scahill mention here:

In one tactic, the NSA “geolocates” the SIM card or handset of a suspected terrorist’s mobile phone, enabling the CIA and U.S. military to conduct night raids and drone strikes to kill or capture the individual in possession of the device.

The former JSOC drone operator is adamant that the technology has been responsible for taking out terrorists and networks of people facilitating improvised explosive device attacks against U.S. forces in Afghanistan. But he also states that innocent people have “absolutely” been killed as a result of the NSA’s increasing reliance on the surveillance tactic.

A “suspected terrorist” could be anybody, even you, or anyone who simply is in the vicinity of your phone. This should absolutely terrify everyone. But not so much so that we are frozen into inaction. Have a little outrage along with that terror. A lot of outrage, even better.

And for good measure, here’s another guide to domestic spy drones: KNOW YOUR DRONES.

A couple of interesting stories read over the weekend about how–not to beat a dead horse (because this horse is very much alive)–everything is rigged, from the “economy” to war.

First a great one from Ellen Brown regarding interest-rate swaps, which were sold to investors (such as the county where I live–Riverside County) on the idea that by buying these swaps, the investors could get cheaper loans with variable interest rates and the swaps would have the effect of making the variable interest rates behave as more or less fixed interest rates thereby supposedly giving the investor the best of both worlds. Brown explains:

“Interest-rate swaps are sold to parties who have taken out loans at variable interest rates, as insurance against rising rates. The most common swap is one where counterparty A (a university, municipal government, etc.) pays a fixed rate to counterparty B (the bank), while receiving from B a floating rate indexed to a reference rate such as LIBOR. If interest rates go up, the municipality gets paid more on the swap contract, offsetting its rising borrowing costs. If interest rates go down, the municipality owes money to the bank on the swap, but that extra charge is offset by the falling interest rate on its variable rate loan. The result is to fix borrowing costs at the lower variable rate.“

As usual, however, the banks found a way to violate this agreement and make it pay for them while simultaneously causing grievous financial harm to the investors. The banks’ method? Rig the interest rates–chiefly LIBOR. Brown quotes an explanation from a CNN writer:

“In 2008 and 2009, Libor rates, in general, fell much faster than the Sifma rate. At times, the rates even went in different directions. During the height of the financial crisis, Sifma rates spiked. Libor rates, though, continued to drop. The result was that the cost of the swaps that municipalities had taken out jumped in price at the same time that their borrowing costs went up, which was exactly the opposite of how the swaps were supposed to work.“

The exact opposite of how the swaps were supposed to work. In other words, the ol’ bait and switch. There’s the way they lead you to believe the world works, and then there’s the way the world actually works, which leads us to the next story, from Empire Burlesque.

Seymour Hersh, Syria, false flags

The Empire Burlesque piece is a commentary on a Seymour Hersh article in the London Review of Books (which is discussed in the video above). The Empire Burlesque writer Chris Floyd states the obvious:

“And that’s another valuable aspect of the Hersh story: it shows, once again, how the world is really run — in almost total secrecy, behind thin facades of hype, hypocrisy and auto-hypnosis that have little or no connection to the reality of power’s operations. Almost nothing we are told is true; yet billions of words are poured out every year in earnest disquisitions on the meaning and import of the dumb shows and distractions our betters put on for us while they pick our pockets and set our world on fire.“

Floyd goes on to point out how all foreign policy is essentially a false flag:

“There is much more in the Hersh piece, including more details on how the administration of the Peace Prize laureate has assiduously pushed policies that it knew, beyond a shadow of a doubt, would result in deadly weapons getting into the hands of some of the most virulent religious extremists on earth. It’s odd, isn’t it? In order to overthrow a repressive regime in Syria, the Peace Laureate allies himself in clandestine gun-running and the fomenting of sectarian violence with a regime, the Saudis, whose repression makes Assad’s Syria look like Haight-Ashbury in the Sixties. And while telling us that al Qaeda is such a deadly foe to all human values that our fight against it requires us to give up our own freedoms, violate our constitution, institute death squads, set up all-pervasive surveillance, and wage overt and covert wars all over the earth — the same Laureate is ensuring that groups openly allied with al Qaeda are being crammed full of weapons so they can spread sectarian violence across the Middle East and Africa.“

Hard to sum up the state of the world any more concisely or poetically than that–our “betters” pick our pockets and set our world on fire–from the unwarranted war of aggression against Iraq to the bailout and other financial frauds such as the foreclosure crisis and LIBOR-rigging, the idea is to leave us broke debt-slaves in a constant state of panic. It’s 1984 all over again.

New mortgage originations fell over 23% month-over-month and a stunning 47% year-to-date according to Black Knight (formerly LPS). As they show in their detailed presentation, with a 65% year-over-year drop, new mortgage originations are at their lowest since their records began and what is perhaps more concerning is prepayment speeds signal further declines are ahead and the ratio of serious deterioration to foreclosure (along with huge numbers of loan mods due to reset) suggest the housing market is anything but recovering fundamentally with the average loan in foreclosure now 2.6 years past due.

People catching on to bank fraud or just broke?

So what accounts for this new low in mortgage origination? Maybe people are finally catching on to the fact that the big banks are essentially criminal enterprises and just don’t want to do business with them. Or maybe people have finally realized, as the Bank of England recently reminded the world, that mortgages are fake–that is, they aren’t “loans” in any common understanding of the usage of that word because banks do not lend deposits, hard money, coins, bills, notes, or any other pre-existing form of money or currency. They just enter digits into a computer database and call that a “loan” that you must pay back with interest.

In fact, it’s worth revisiting one of the most startling (at least to those who adhere to the conventional “wisdom”) quotes from the BoE’s recent press release (which applies to banks all around the world, including the United States) which explain and confirm that banks do not lend deposits or pre-existing money:

“When a bank makes a loan, for example to someone taking out a mortgage to buy a house, it does not typically do so by giving them thousands of pounds worth of banknotes. Instead, it credits their bank account with a bank deposit of the size of the mortgage. At that moment, new money is created.”

No, actually at that moment, you’ve been bamboozled. Hoodwinked. As David Graeber pointed out, this admission–which has never been hidden or secret, it’s just not widely known to the public (because of disinformation, of course)–certainly destroys any rationale for the austerity programs that the banks are trying to enforce. But it also destroys any rationale for not having a complete debt jubilee all across the world and completely restarting with a new system. More on this in a future post.

But the more likely answer to the record-low mortgage originations is that people are just broke, unemployed or underemployed, and/or have horrible “credit scores.”

And a credit score by the way, in light of the above info about how money is actually created, is not really a measure of the risk a bank will take in “lending” a person money. That’s because there is no risk for a bank when it “lends” a person money because the banks, as explained above, do not lend money–they enter numbers into a computer and call it a “loan”. But again, that’s a topic for another day. So, I’m going with “bad credit”/broke/un-or-under-employed as the reason for the lack of mortgage originations: