I won’t mince words: banks are financial terrorists (Max Keiser explains why in the clip above). Always have been, always will be until we start thinking of them as what they are–i.e., terrorists–and acting accordingly. So what is this claim of terrorism based on?

Well, courtesy of attorney Dale Wiley, out of Missouri comes the case of Feeney vs. Nationstar. Long story short: the Feeneys filed bankruptcy and in the midst of it began to think that the corporate entity that purported to be able to foreclose on the Feeney’s house did not actually have the right to do so. So they started asking questions and y’know, defending themselves on the basis of sound legal principles like negotiation and the Uniform Commercial Code. The Feeneys were wise to what was going on, and turns out they were totally right to bring up the questions they did because they had caught the bank with its pants down. The bank didn’t have the authority it claimed it did, so then what happened? Quite reflexively, as easy as you please, the bank manufactured the evidence out of thin air–just like they do with money!

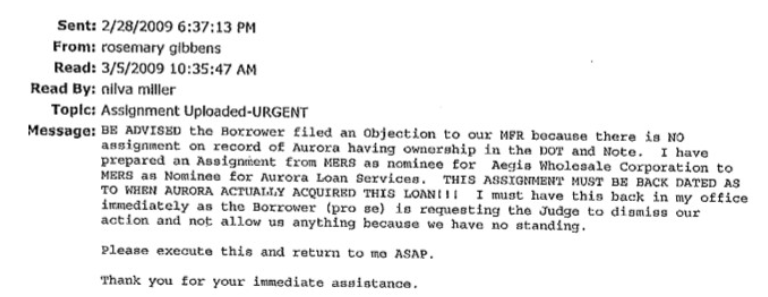

Proof the “evidence” was manufactured

This kind of manufacturing of evidence happens all the time, it’s just that usually, hard evidence of this criminal behavior is hard to come by. However, Wiley got undeniable proof of it this time. He got his hands on a Nationstar (who used to call themselves “Aurora”) internal memo which said this:

So the Feeneys were right–there was no assignment that gave Aurora/Nationstar the right to do anything. SO THEY (AURORA/NATIONSTAR) MADE ONE UP, BACKDATED IT, AND GOT A NOTARY TO SIGN OFF ON IT! And then filed it in the land records of Greene County, Missouri!

Why did Aurora/Nationstar do this instead of just admitting their mistake? Why, to screw over the Feeneys, of course! That’s the whole point of all of this: the banks must screw the American public out of their property, even if they have to cheat to do so—EVEN IF THE BANK HAS NO LEGAL INTEREST IN SAID PROPERTY! Hell, especially if they have no legal interest in the property!

And you know what? IT TOTALLY WORKED! The bankruptcy court took the manufactured evidence, blessed it, and said to the Feeneys, “You poor bastards are gonna lose your house because ta-da! Here’s the assignment you wouldn’t shut up about! Are ya happy now?”

The REAL paper terrorism

But when someone like Barbara Bratton engages in this same exact behavior, she gets thrown in jail and accused of engaging in “paper terrorism.” Same with Howard Graber, who is facing 170 years in jail because he did the same thing.

But you know what Bratton and Graber and others like them were doing? They were defending their property, property they knew the banks didn’t own and had no interest in, despite the bank and/or their goons (i.e., “servicers”) saying otherwise. And both Bratton and Graber tried to get satisfaction in the courts, but the courts wouldn’t hear of such. Bratton’s case was dismissed without discovery, and Graber was forcibly evicted by a SWAT team despite having filed a counteraffidavit, which under Georgia law meant that he should have been allowed to stay in his house and be allowed a jury trial on the merits.

And then Bratton and Graber are labeled as terrorists and fraudsters, all because they tried to defend themselves and their property. But isn’t that what Americans are supposed to do–defend themselves? Defend themselves from criminals and thieves? And aren’t the criminals and thieves the real terrorists? Of course! The banks that do this kind of stuff are the real terrorists and it’s time we all–the courts, the media, and the public–start thinking of them this way.

Karen Pooley, long-time crusader against foreclosure fraud, recently won her motion over whether or not her adversary can claim work product privilege over some important documents. She sought what is known as “in camera” review, which is when a judge reviews evidence to determine whether or not it should be provided to all parties to the lawsuit. The judge seems willing to rule in her favor on this–and only this–matter. Indeed, he pointedly cuts Pooley off when she brings up the f-word: fraud. To be fair, though, the judge does indicate that he would be willing to discuss the fraud accusation further if his review of the documents in question warrants such discussion (fingers crossed).

But Pooley clearly has a strategy going here: fight them on and for every last little thing. Fight them and never give up. Nothing you can do is insignificant. Spoon-feed your case to the judge in the smallest possible bites he can swallow, and then, slowly but surely, he’s eaten it all up! Brava, Ms. Pooley, Brava!

Don’t count on it, but it would be great if they would. And there is a petition for a writ of certiorari in the case of Duncan K. Robertson v. GMAC Mortgage LLC et al. which could have that effect. Below are a couple of great quotes from Scott Stafne’s petition:

“It is inappropriate for the federal District Court of Washington to continue chastising borrowers by claiming federal courts do not accept any “show me the note/split the note” defense when Wash. Rev. Code § 61.24.030(7)(a) and the Washington Supreme Court indicate otherwise. Indeed, even this Court has recognized the viability of this defense. See Carpenter v. Longan, 83 U.S. 271 (16 Wall. 271), 21 L. Ed. 313, (1873). As does the Restatement of the Law, Third, Property (Mortgages) 5.4 when an intention to split the note can be proved.”

Well said. There is a tendency of federal district courts (and not just in Washington)–a very strong tendency–to discount the very clear dictates of Carpenter v. Longan. See, for example, the Texas case of Kramer v. FNMA, which I wrote about in a post titled MERS IS THE PROBLEM, PART 5 MILLION AND COUNTING… In Kramer, Judge Sam Sparks said that when Carpenter talks about assignments of mortgage separate from the note being a nullity, that is merely “dicta” and Sparks doesn’t have to follow it.

The Supreme Court badly needs to clarify whether it means what it said in Carpenter (i.e., “An assignment of the note carries the mortgage with it, while an assignment of the latter alone is a nullity.”)–or not. A lot of heartache, money, time, and effort could be saved by homeowners, courts, and attorneys if the Supreme Court would simply take up this question. And that’s probably why they won’t hear this case…

Like Bill Butler, Stafne’s petition also makes note of the federal judiciary’s VERY strong tendency to dismiss cases involving financial instruments:

“In 2011 the Federal Judicial Center commissioned a report to determine the effect of Iqbal on dismissals. Cecil, Joe, et al.Motions to Dismiss for Failure to State a Claim after Iqbal: Report to the Judicial Conference Advisory Committee on Civil Rules (2011) (FJC Report). The Report compared dismissal rates under FRCP 12(b)(6) motions to dismiss pre- and post-Iqbal/Twombly pleading standards in order to determine its impact. While dismissal rates were somewhat higher generally, one class of cases – those involving financial instruments – showed that in 2010 federal courts applying the Iqbal/Twombly dismissed 91.9% of financial instrument claims for “failure to state a claim.” This is nearly double the rate of such dismissals (47%) for 2006, pre-foreclosure crisis. Report at 14, Table 4. Notably, the statistics excluded pro se plaintiffs which would have undoubtedly moved the number higher. FJC Report at vii.”

“…in the vast majority of cases, Bank of America (and this goes for virtually all “The Banks”) do not own the mortgages that they are foreclosing on. I have repeatedly used the phrase,

THE WIZARD BEHIND THE CURTAIN TELLS BANKS TO FORECLOSE ON AMERICANS, THE WIZARD OWNS THE MORTGAGES

But here’s the thing….

There’s not just a Wizard Behind The Curtain, There’s an Overlord Behind The Wizard

Fannie and Freddie of course do not own the interests in the notes and mortgages unencumbered….parties that sit behind The Wizard own those interests….but don’t take my analysis standing alone….read what Fannie directly says:

The mortgages that back a Fannie Mae MBS are held in a trust on behalf of Fannie Mae MBS investors and are not Fannie Mae assets.“

That last red part is what we here at Liberty Road Media referred to in the following posts:

Weidner then fingers China as the “Wizard” and/or the “Overlord”:

“So what did China start doing….in record volume purchases? They tied their purchase of US financial instruments to secured interests….they took collateral. That collateral?

The mortgage on the homes that judges are foreclosing on all across this country.”

“Could real estate on American soil owned by China be set up as “development zones” in which the communist nation could establish Chinese-owned businesses and bring in its citizens to the U.S. to work?

That’s part of an evolving proposal Beijing has been developing quietly since 2009 to convert more than $1 trillion of U.S debt it owns into equity.

Under the plan, China would own U.S. businesses, U.S. infrastructure and U.S. high-value land, all with a U.S. government guarantee against loss.”

As Weidner facetiously asks: “….what could possibly be wrong here?”

The argument against raising the minimum wage that one encounters quite a bit on social media and forum/blog comments goes something like this: if and when minimum wage is raised, it only makes the cost of goods and services go up for everyone and that this inflation actually then hurts the very people it was supposed to help—namely, the minimum wage worker—because it prices them out of a job (employers can’t or won’t pay the new minimum wage and will cut jobs or go out of business rather than pay the increased wage). Therefore, the argument goes, minimum wage should not be raised. It’s a neat trick, really, arguing that an increase in pay not only doesn’t really help you, Mike and Minnie Minimumwage—it actually hurts you, so really we would be doing you a big favor by not raising your pay. Mike and Minnie, the argument goes, get to keep their jobs that they are lucky to have in the first place (because they’re “unskilled” buffoons), and prices of goods and services don’t rise above their means. Win-win.

Notice that such an argument is never trotted out when news of exorbitant CEO raises (McDonald’s, Chase) or executive bonuses (bailout-era bonuses) comes out. The same people that say raising pay for minimum wage workers hurts those same workers will, almost without fail, say that the CEO/executive pay has been earned by the “skill” and “knowledge” of these CEOs and is deserved and therefore is completely justified. This argument completely ignores reality, as in the recent case of Jamie Dimon, who was just granted at 74% increase in pay despite the fact that Chase bank was hit with billions of dollars in fines in 2013 and may have to admit to wrongdoing in the Madoff matter. If a McDonald’s fry cook were to incur billions of dollars in fines for McDonald’s, would anyone seriously argue that the fry cook would still have a job, much less get a raise? Yeah, and monkeys might fly out of my….you get the picture.

But the point is, these people do not generally argue that CEOs are hurt by pay raises, yet have no problem saying with a straight face that the minimum wage worker is hurt by pay raises. It’s surreal, actually.

Destroying the argument

But let’s say these anti-minimum wage people won the argument. Let’s say that minimum wage right now, in 2014, is the same as it was in 1986, when I myself worked as a McDonald’s fry cook. The minimum wage then was $3.35/hour. That is what the anti-minimum wagers want, right—no raises in the minimum wage (and actually that’s their kinder, gentler argument—lots of them really think there should be no minimum wage at all)? So let’s pretend that Minnie Minimumwage is, right now, making $3.35 an hour. The anti-minimum people would be very pleased, I’m guessing.

But, would their argument have been borne out? That is, would prices of goods and services have remained constant since 1986 all because the minimum wage never went up? After all, that’s the argument—that increased labor costs are the primary driver of both inflation and unemployment. Would jobs be plentiful and prices be low if the minimum wage had not increased since 1986 (i.e., in 28 years)?

The answer, of course, is: are you shitting me?

Now who’s being naïve?

We now have admissions that markets and prices are rigged, and have been for a long time. The idea that American business runs on a junior-high textbook model of “prices are set by supply and demand” is incredibly naïve. That is, prices do not automatically and inevitably go up simply because labor costs may have risen by a dollar an hour. Prices are set independently of such things—in short, prices are manipulated and rigged and the minimum wage has little or nothing to do with it.

So minimum wage is the LEAST of our worries when it comes to getting ripped off and/or suffering inflation and unemployment. Indeed, until all this rigging of the markets is stopped, minimum wage has got to be increased. I don’t support Obama and don’t want to agree with him on anything, but on at least this one issue, I have to say he’s right.

The Grabers received a call today: their trial set for Monday, January 27, 2014 has been continued. Meaning, no trial Monday! Keep up the pressure, keep up the good fight. Good things are a-brewing! Feel free to add your signature to their petition: “Don’t Convict Disabled Howard A. Graber, He Is A Victim Of Foreclosure Fraud!“

Story by: Clinton Kirby Published: January 24, 2014

In his upcoming trial this Monday, January 27, Howard A. Graber faces 170 years in prison for 10 counts of what the state of Georgia has called “mortgage fraud” and “forgery.” That is almost two centuries of imprisonment, more time than he’d get if he’d killed someone. But he didn’t kill anyone. He didn’t hurt anyone. He never lifted a hand against anyone. So if he is facing more jail time than a first-degree murderer, he must have done something awful, right, like worse than murder?

The answer to that question: hardly. Of course not. Hogwash.

What he did is try to save his home from foreclosure after losing a lucrative job as a Network and Sales Engineer, suffering a debilitating stroke, and trying to make it on just his disability income. He had sued M & T Bank to stop the foreclosure but to no avail, as detailed here:

“Lateef Bey, an associate who met the couple in homeowners and foreclosure protection meetings, said they’d filed a counter-affidavit* in Gwinnett State Court in the belief they’d been denied due process.

A copy of that document was taped to the Grabers’ front-door and sent to high-ranking sheriff’s department officials, Bey said. By forcefully entering the home, Bey feels deputies exceeded their authority and failed to abide by Georgia code.

‘I think that this is a very sad day. Tomorrow it could be your home,’ Bey said. ‘We live in a state of tyranny if we can’t get our rights enforced.’”

So in a typical display of police-state gross overreaction, a SWAT team was sent to evict the Grabers from their home in Duluth. What followed was an hours-long standoff between a locked and loaded SWAT team and a disabled man and his caregiver wife. Upon entering the Graber house, Graber’s wife Nova-Lee was tasered, according to news reports.

Unfortunately, this has become the new “normal”: breadwinner loses job, has health crisis, falls behind on mortgage, bank ultimately doesn’t do anything to help out the homeowner, the courts don’t either, so broke, frustrated, disabled, scared homeowner gets forcibly evicted by men with machine guns. OK, wait a second-maybe that very last part about the men with machine guns isn’t so typical. Most people in the Grabers’ situation just hang their heads and walk away in shame and the SWAT team never has to step one jackboot out of their armored vehicles.

But that’s what separates the Grabers from most people facing foreclosure and helps explain why the state of Georgia is coming after them like the hounds of hell: they fought back. And the individual who will stand up for himself or herself is the biggest threat the state faces. That can’t be allowed—examples must be made.

The documents tell the tale—or do they?

Now comes the part of the Grabers’ story where some people may be tempted to withdraw their sympathy and understanding. This is the part where the Grabers dared to do what the banks do all day long, every day—file documents of dubious legality in the county land records. These documents were filed in January 2010, almost 8 months before the Grabers’ run-in with the SWAT team, with the exception of amendments to two of the documents, which were filed in November 2010.

So what were these documents that the Grabers dared to file? Without getting too specific, the documents were styled as a satisfaction of the Grabers’ mortgage, reconveyance of the property to the Grabers, and so on. And these documents were signed by Graber himself as an agent of M & T Bank, the lender named in his promissory note.

At this point, one might well ask: why shouldn’t Graber be punished for filing such documents? After all, if all one has to do is take it upon oneself to file a satisfaction of mortgage which purports to be from one’s lender, what’s to stop everyone from doing that? The banks would never get their money back! Almost two centuries in jail is too good for Howard A. Graber!

The banks do it, no problem

Well, aside from the issues involving the fact that all banks create money out of thin air and that what we currently call “promissory notes” are really checks from borrowers to lenders rather than the other way around, there’s this small problem: the banks do this stuff all the time. Case in point—Lorraine Brown of DocX.

According to the New York Times, Brown “admitted to participating in the falsification of more than a million documents.” Yes, you read that right–she participated in the falsification of more than one million documents. And these documents were produced at the behest of banks that hired Brown and her company to produce admittedly false documents that were then filed in county land records all over the country and used as evidence in court cases.

In other words, Howard A. Graber only did what Lorraine Brown did. But he did it on a much, much, much smaller scale. And he only did it with documents pertaining to his own home.And, as will be discussed below, there is a legitimate argument that Graber’s documents are not false, thereby creating reasonable doubt in his case. So is Lorraine Brown going to jail for 170 years? Do we even have to ask? No, Lorraine Brown will not be serving 170 years for falsifying over one million documents—that was never even in the cards (from the same New York Times article):

“In the federal case, she could face a minimum of probation and a maximum of five years in prison. In the Missouri matter, she could receive a sentence of two to three years. But if she receives a federal sentence of probation or fewer than two years in prison, Mr. Koster said, she would be obligated to serve at least two years in Missouri.”

Well, as it turns out, she got the maximum sentence: 5 years in prison for the federal offenses and two 3-year sentences in Missouri that she will serve concurrently with the federal sentence. Not even close to 170 years.

What the hell? Or, why not 5 million years?

So what have we learned, then? What is our illegitimate corporate government trying to “teach” us in all this? Well, the lesson I take from it is this: if you’re gonna commit fraud on the land records, commit a really gigantic fraud because if/when you get caught, you’ll get 5 years at the most. It seems that if the goal of our corporate state were to offer equal protection of the laws, then Lorraine Brown would be facing a geologic era in prison: over 5 million years; 5 years for each falsified document. But no, she’s only getting 5 years while Howard Graber faces 170 years.

There is reasonable doubt that Howard Graber committed fraud

And for those who might have the sneaking suspicion that Howard Graber committed fraud by filing his various documents in the land records, I say: prove it. Is Howard Graber (or anyone else, for that matter) any more or less of an agent of M & T Bank Corp. than an employee of M & T Bank’s alleged servicer who would call themselves a “vice president” of MERS when doing an assignment from M & T at the time of foreclosure? I mean, in real terms, Graber is no more or less of an agent than that “vice president,” but Graber gets charged with crimes while the MERS/M & T “vice president” has nothing to worry about.

Furthermore, given the myriad known and admitted problems with securitization (for starters, see this,this, and this) did M & T Bank actually have any interest at all in Howard Graber’s house? Did they or their agent or assignee or successor-in-interest actually hold Graber’s promissory note and/or have the right to enforce that promissory note? That’s a perfectly legitimate question, and one that should damn well be answered before Graber is thrown under the jail for 170 years. The only way that Howard Graber can be said to have committed “mortgage fraud” is if the documents he filed are actually false. And proving that Graber’s documents are in fact false is what the state of Georgia should have to do. That would be very interesting to see: can the state of Georgia prove, beyond a reasonable doubt (the standard in a criminal case), that M & T Bank—or any bank or investor—had a legitimate, properly-documented interest in Howard Graber’s house?

And the answer to that is: hell no, the state of Georgia can’t prove that beyond a reasonable doubt. No one can. Indeed, given that Lorraine Brown’s company DocX (you know, the one that admitted to putting over a million falsified documents into the public records) was located in Alpharetta–which is right next door to Graber’s town of Duluth–how can we know for sure that Graber’s chain of title wasn’t poisoned with fake documents produced by DocX? Are we to believe that DocX, a local Georgia company, never got called on to commit document fraud in places where they could send falsified documents over by bike messenger? Come on—that beggars belief. And by the way, as an aside, let us point out here that when Lorraine Brown admitted to falsifying over a million documents, that could mean (and almost certainly does mean) that 10 million documents were falsified. Or 20 million. Or many more. Notice that you never hear about the top end of the estimated range of falsified documents—just the bottom end.

It is the banks who are committing the fraud and desperate to steal

So in the end, we can easily see that it is the banks—and not homeowners like Howard Graber—who are desperate to steal homes and defraud the land records. Indeed, the banks know full well that fraud and falsified documents are the only way they can foreclose. There is no other explanation for why they would do it, and do it on a scale which is orders of magnitude greater than Howard A. Graber could ever think about doing. Not only that, this paper terrorism of the banks via DocX is openly admitted. Yet Howard A. Graber is the one who faces 170 years in jail because he knew about the bank fraud and tried to do something about it.

Would I have done what he did? No, I wouldn’t have. Would I recommend anyone else doing what he did with the land records? No, I certainly wouldn’t. At this point, I don’t think even Howard A. Graber would recommend doing what he did, and he shouldn’t have had to even contemplate doing it. But many others have done what Graber did. Some of them are facing adverse consequences like Graber (Barbara Bratton in California comes to mind), yet some of them are not.

And the point is, something has to be done. The banks are openly committing mortgage fraud and the courts are allowing it (with so few exceptions to that rule that it’s hardly worth mentioning). People are losing their homes and their livelihoods in this bank crime spree and the powers that be should be glad that all people are doing so far is trying to use paper (whether in the courts or in the land records—or both) to get their property back or keep it, because the alternative is very ugly for everyone involved. Howard A. Graber at least had the courage to do something about being ripped off and he obviously does not deserve 170 years behind bars.

Graber summed up his situation thusly: “The most important thing you have to recognize in all of this is how Georgia—a non-judicial state–has shut the doors on due process.” Frankly, he’s right, and the last part of that statement applies to the entire country–the doors to due process have indeed been shut, padlocked, welded together, boarded up, and then fitted with booby traps. But only for homeowners. The doors to due process for the banks are wide open. Hell, the doors to “due process” for the banks have been taken off their hinges and the doorframe widened to accommodate the biggest possible amounts of fraud and deception the banks want to bring in. Is everybody OK with that? Howard A. Graber wasn’t and isn’t. God help us.

*Excerpt from Georgia code: “O.C.G.A. § 44-11-32 – If the party in possession submits a counter affidavit as provided in Code Section 44-11-30, the Sheriff shall not turn him out of possession but shall leave both parties in their respective positions. In such an event, the Sheriff shall return both affidavits to the office of the clerk of the superior court of the county in which the land is located for a trial of the issue before a jury in accordance with the laws of this State.“

How you can help:

Graber’s trial is this coming Monday, January 27, 2014. Tell Judge Warren Davis to let disabled Howard A. Graber go!

Judge Warren Davis Phone:(770) 822-8041 Fax:(770) 822-8535

Below is a press release from Karen Rozier, a woman fighting foreclosure and now for her freedom. Unbelievable.

HAPPENING TOMORROW MORNING Jan. 14th 8:30 AM IN DOWNTOWN LA COURT DEPT. 45, 7TH FLOOR

Media Contacts: Pam Ragland, (949)734-0374, Pamcl@AimingHigher.com Karen Rozier, rozier.karen@yahoo.com;

LA City Attorney May Jail Foreclosure Fighting Family Tomorrow Morning, After Refusing To Admit Crucial Evidence

LOS ANGELES, Calif. – Jan. 13, 2014 – Is it just a coincidence Harvard University alumni Karen Rozier, and her unlicensed Cal-Poly Pomona degreed architect husband and Eagle Scout David Rozier, Sr., now find themselves wrongfully convicted of being ‘uneducated’ and ‘unqualified’ and facing jail—while fighting two of the biggest banks in the United States? Or do Bank of America and US Bank (U.S. Bankcorp, N.A.) have way too much influence to shut down wronged homeowners in this “Too big to fail” banking climate?

“We had no idea our Public Defender’s son works at Bank of America”, commented Karen Rozier. She also pointed out Judge Renee Korn, seeing a conflict with their criminal trial, promised to call the judge to postpone a critical US Bank ruling. “Yet, when I spoke to Rick Burns, he claimed he had never once heard from anyone from Judge Korn’s courtroom, and no such call ever took place to Judge Fell’s courtroom.” This caused US Bank to admit all of their facts into evidence, and Karen Rozier has never made one allegation against U.S. Bank, Bank of America and GMAC Mortgage already admitted to their mistakes, but U.S. Bank is trying to bury the truth — and the Roziers.

When former client Chona Ekstrand ran out of money for a potential building project, she asked for a refund on work the Rozier’s completed, including the work they completed while their son was fighting for his life in Children’s Hospital Orange County. When the couple refused, Chona Ekstrand used her connections in Los Angeles—despite the fact the African American couple lives in Orange County—to claim the Roziers aren’t who they say they are. She accused them of being “ghetto”, and lying about their education, in open court. Yet, although central to the case–the court refused to admit the Rozier’s education and credentials into evidence or to allow them any witnesses –so the jury never heard it.

The Roziers – an Orange County, Calif. couple “famous” for fighting US Bank, Bank of America, and GMAC Mortgage over the wrongful foreclosure of their home — have been battling the LA’s City Attorney in this fouryears-long case. However, the timing is suspect as their trial suddenly got scheduled just as the Rozier’s had a major hearing against US Bank and are preparing finally for trial. Besides Judge Korn neglecting to contact the court to postpone the US Bank hearing—she also refused to admit crucial evidence such as Karen Rozier’s educational background, or allow the many neighbors ready to testify David Rozier built their home himself just as he claimed. Karen Rozier also has an advanced degrees from Carnegie Mellon University. Instead, Judge Korn allowed the jury to hear LA city attorney Keith de la Rosa accuse the Rozier’s of being “ghetto”, “nothing”, “liars”, “con artists” and assert his claims they had “lied” about their abilities. The implication is they could not possibly have the education they claim. Yet the jury, without access to the fact Karen Rozier has three college degrees– including earning a bachelor’s of science in electrical engineering and a master’s of science in industrial administration from Carnegie Mellon University, and a master’s degree in public administration from Harvard University—was left to believe the LA City’s depiction of her as “ghetto” and “uneductated”. Typically entering key evidence relevant to the charges into a trial is allowed.

Karen Rozier then made transparent the connection between the court-appointed counsel – who Ms. Rozier met for the first time at trial — and Bank of America. His son works for Bank of America in the Corporate finance Department—just a few blocks from where the Roziers were convicted. Normally with such a conflict of interest, he should have withdrawn. “Bank of America sold a rescinded loan to investors and to US Bank, who is attempting to foreclose on it. I was paying on the valid loan when GMAC Mortgage attempted to foreclose on the rescinded loan. GMAC Mortgage rescinded the foreclosure and that should have been the end of it. The loan does not exist, and there have been many times the two banks joined forces to hide this fact as this is also securities fraud. Their attorneys even forget who they are representing!”, Karen Rozier noted.

US Bank had already previously succeeded in using fraudulent emails to accuse the Rozier’s of being “dangerous”. The judge in that case, Judge Scott Steiner –who was under indictment for having sex with a staff member in exchange for a job–ruled against the Rozier’s and issued an order to take their guns [READ THAT STORY HERE]. “I was in the courtroom and heard the tape. Ms. Rozier threatened to have the lawyer arrested to breaking the law! That judge refused to admit the tape, even though it was U.S. Bank’s evidence! You have to ask ‘why’?”, said Pam Ragland, another homeowner successfully fighting US Bank, and who was made famous last summer for finding a missing boy in Riverside.

During the trial, the embattled couple’s stellar resumes were questioned, without allowing them to enter their education and experience–thereby backing up the prosecution’s case the couple somehow ripped off this former client, which the Roziers patently claim is false. “We absolutely did the work and she even admitted that she refused to accept the product.” says Karen Rozier. “She lost interest in the project after she lost her job and her HELOC dried up.” she adds.

Karen Rozier’s stellar education is coupled with her 5 years with the Naval Air Systems Command, and her two years at the Naval Sea Systems Command. She led the performance assessment branch for Missile Defense. So—not only is she educated, but she could most certainly be called a “rocket scientist” The Navy even invited her back to assume the position of Chief Engineer, Air-to-Ground Missiles. She lost that career-defining and well deserved position due to the LA City Prosecutor’s charges, which hinge on the fact she wasn’t as educated as she claimed, since the position requires a security clearance. As for David Rozier – neighbors stood ready to testify he built the couple’s 4,206 sq. ft. Buena Park home himself, something the prosecution denied and was pivotal to the Rozier’s defense. After all, they were simply claiming they had built their home under the average price per square foot. Ironically, this is the same home which is the subject of the lawsuits against US Bank, Bank of America, and GMAC, for their continual attempts to foreclose on a non existent note, once describing the Rozier’s home as a 1500 square foot one-story home. All this has left the Rozier’s to wonder how these “too big to fail” banks could have manipulated these proceedings.

Tomorrow as this American super couple goes back into court today at 8:30 A.M. in Dept 45 on the seventh floor of the city’s 210 W. Temple Ave. court, the Roziers say: “We were convicted for claiming to be what we are — talented and educated.” The couple is requesting a new hearing, to allowing the suppressed evidence to be heard. Members of the media and the public are encouraged to both call and stand witness in the courtroom to send a strong message to the banks and bad judges: “Please restore my faith in justice. Allow a new hearing for David and Karen Rozier. If not for Justice, then for David. Jr.” (213)974-6015

Today Neil Garfield gets into the fact that the courts are rigged. Yeah, I know–no shit, Sherlock. He has this to say:

“Citizens who find themselves in the court system are fast losing faith that it is a rubber stamping system if they are accused of anything, and an obstacle to justice if they are seeking compensation for damages sustained as a result of breach of duty or obligation.

[BIG SNIP]

The very people who should be an army of revolt in the Courts are so intimidated by their opposition and what they see happening in the courts that they give up their largest investment, their lifestyle, their neighborhood because they are demoralized by a rigged legal system.”

Indeed. No question about it.

Why is everything rigged?

But for whatever reason, this article made me ask why everything is rigged. I mean, on the surface we know why: for political control, for financial gain, for raw power, etc. Yes, of course.

But here’s the angle I hadn’t really thought much about before–just follow with me for a moment. It’s the rich and powerful, by and large, who are participating in this rigging, right? After all, they’re the only ones who can really rig the game to begin with.

And we are told, over and over, that these rich and powerful types get to be rich and powerful because they are, in a word, better than us. Or smarter. Or just more talented. That kind of thing. Here’s the rub, though–if they really are better, or smarter, or more talented, why do they feel the need to rig the game? Wouldn’t they become rich and powerful anyway, merely by dint of their being better, smarter, and more talented?

Oh, that’s why

Well, apparently not, otherwise there’d be no need to rig everything. Indeed, if the banks could really prove they owned your house, they wouldn’t have to manufacture documents, as they admittedly have. If people really wanted gas-guzzling cars, there would have been no need to take the electric car off the market. If the pathetic candidates that constantly get “elected” could do so without massive election fraud, there’d be no need for black box voting. There’d be no need to rig prices and manipulate markets. And so on.

So in a very real way, the fact that everything has to be rigged in the favor of a few insatiable, greedy monopolists is a testimony to the power that we all have–because we are infinite consciousness as David Icke talks about in this video:

The fact is they’re not better. They’re not smarter. They’re not more talented. And they know it! The only thing they’re better at is rigging things, which when you think about it, really isn’t a skill. Hell, if we’re running a race and I trip you and I end up winning, my victory is not due to the fact that I was faster than you. I won because I tripped you and you had to take extra time out of the race to recover from your fall, not because I was a better or faster runner.

But they are smart enough to know that if they don’t rig everything in their favor, they won’t have power or wealth. They’ll be nothing. And so in fact, in the final equation, they are nothing. And it is up to us–the ones they’re so scared of–to finally and always treat them that way.